[E3.1] Disruption according to Wright: Y = aX^b

Can a formula drive market leadership?

Dear Reader,

Yes, for this profile in Product | Strategy | Innovation, we explore a formula to help us better understand our world and its technology companies. Welcome to enlightenment. This formula in particular helps us model 2 key attributes of innovation. The first is the cost to produce the first unit with commercial production. And the second is the rate cost per unit decreases as production scales. Both attributes impact how a product is positioned in the market based on price, but operating leverage associated with the latter can accelerate taking market share, improving profit margins and higher income from operations. This is illustrated in Fig. E3.1-1 for Tesla where the year-over-year increase for a recent 1-year period is proportionally greater going from Total Revenue (39%) to Gross Profit (73%) to Income from Operations (210%). The degree of operating leverage for this time period can be calculated using the proportional increase in Income from Operations divided by the proportional increase in Total Revenue, or 210% / 39% = 5.4 in this case. That translates into $5.40 in extra income for every $1 in incremental revenue. As operating leverage increases this ratio expands further.

High operating leverage does come with risks. It requires investments in fixed costs associated with building & operating factories, vertical integration, product research & development, process innovation, human capital, etc. If market demand and pricing drive sustained revenue growth, the impact can be quite dramatic on higher income form operations. This can be seen in software and pharmaceutical companies. But if revenue drops, the negative impact on income is also dramatic.

You may have heard about Moore’s Law that has described innovation in the semiconductor industry for many years.

We will explore the following in this profile:

Moore’s Law vs. Wright’s Law

Ford & Tesla according to Wright

Autonomous Vehicle Navigation

Is Moderna the Tesla of biotech?

If you are not a subscriber to Product | Strategy | Innovation, please consider doing so for updates like this one and more.

1. Moore’s Law vs. Wright’s Law

Gordon E. Moore co-founded Intel Corporation, but prior to Intel he made the observation in 1965 while at Fairchild Semiconductor, the number of transistors incorporated in a microchip doubles every 12 months. This increase in transistor density not only led to increasing performance, but reductions in cost as well. In the mid-70’s this rate of doubling slowed somewhat and Moore’s Law was revised to state the number of transistors doubles about every 18-24 months. This ability to forecast semiconductor properties allowed Intel and other semiconductor companies plus their customers like IBM, Compaq and Dell to make significant capital investments into the research & development required to realize the commercial upside from market growth with lower costs and increasing performance. These companies were able to model the future using price elasticity to understand market demand vs. product roadmaps. Customers and investors also benefitted. But Moore’s Law has started to falter over the last 15 years as demand has not driven the same pace of innovation. Time seems less reliable to model unit performance and unit cost.

Theodore P. Wright predated Gordon Moore, but had similar interests as an aeronautical engineer and educator to understand airplane manufacturing. Wright made the observation in 1936 that cost declines as a function of cumulative production. For every cumulative doubling of units produced, costs will fall by a constant percentage. Wright’s Law can be written using the formula

Y=aX^b

where:

Y = cumulative average cost (or time) per unit

X = cumulative number of units produced

a = cost (or time) required to produce 1st unit

b = slope of the function

Cumulative production as the independent variable (X) with Wright’s Law outperforms Moore’s Law over long time periods based on a study across multiple industries and 62 different technologies.

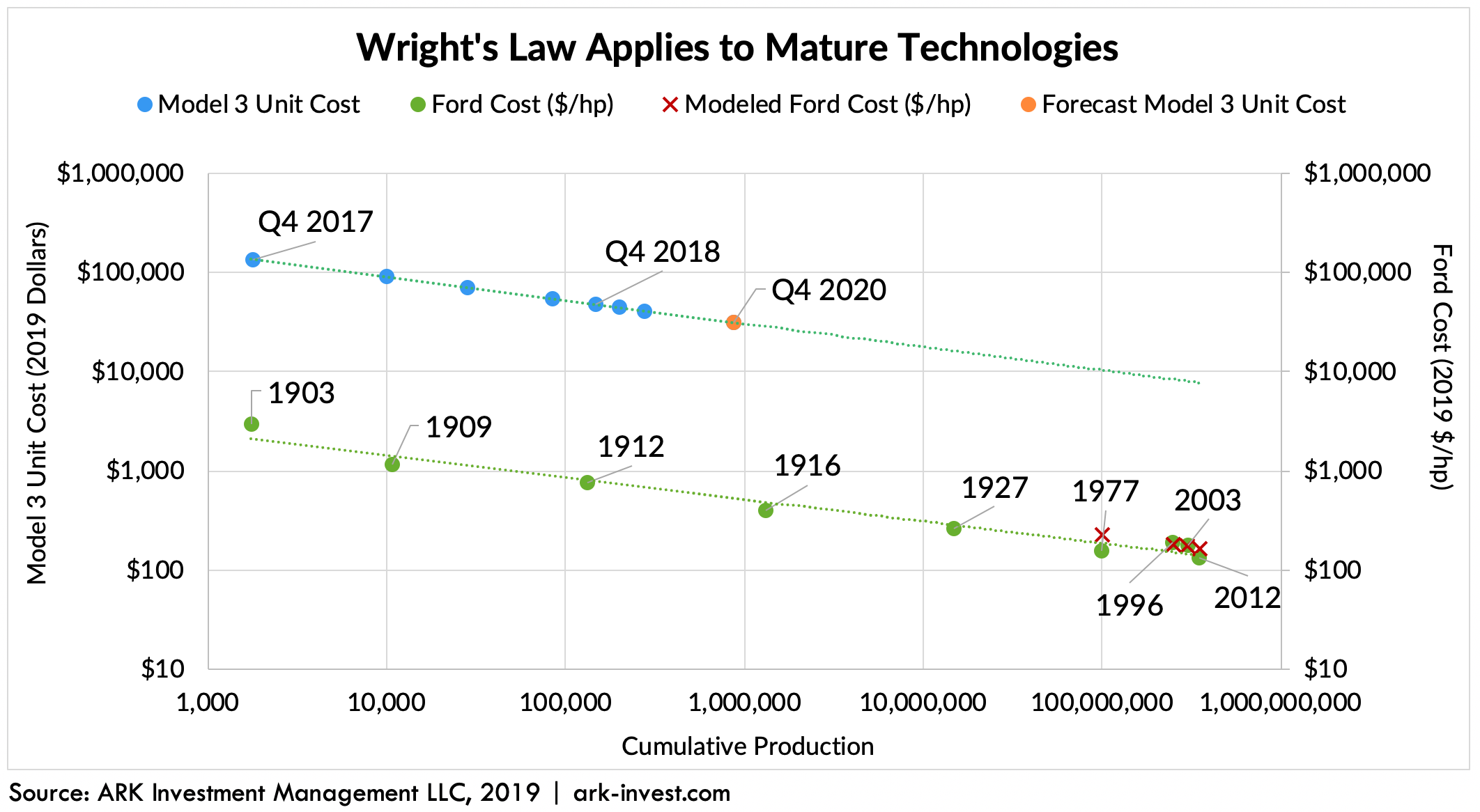

2. Ford & Tesla through the lens of Wright

Ark Investment Management LLC (aka Ark Invest) is a global investment firm that focuses on disruptive innovation, thematic analysis and openly publishing their research to build relationships with subject matter experts. This leads to an evolving ecosystem around thematic areas of interest like artificial intelligence, robotics, blockchain, energy storage and DNA sequencing. Ark Invest modeled the automobile industry for over a century starting with Ford’s Model T vehicle production in 1903. The model continued through later models with 350 million cumulative units produced by 2012 over a 109 year period. Even with many changes in technology and processes, Wright’s Law holds up well as shown in Fig. E3.1-2 with the green dots and linear relationship for Ford (unit cost/horsepower vs. log cumulative production). Please note that cumulative production on the X-axis is a logarithmic scale, but the Y-axis is a linear scale for unit cost (2019 dollars per hp).

Also, note that when the Tesla Model 3 estimated unit cost shown with blue dots in Fig. 3.1-2 is modeled on the same chart starting in Q4 2017 and partially through 2019, it starts at a higher unit cost in 2017 than the Model T per hp in 1903 (using 2019 dollars). Unit cost decreases linearly with cumulative production on the same logarithmic scale and proportionally to Ford over a shorter time period. Tesla’s cumulative production in 1 year required 9 years for Ford over a century ago. This is likely a result of both increased demand and more automation today. But Wright’s Law shows very similar characteristics.

This also shows Tesla should be able to reach an estimated $10,000 Model 3 unit cost with 100 million cumulative units produced. But that is the Model 3. Tesla is working on a lower priced vehicle in Shanghai and Berlin for those markets at a rumored $25k base price. That means the cost to produce the first unit (“a” in the formula) should be less than the Model 3, but if it decreases proportionally (“b” in the formula) to the Model 3, it would reach a $10,000 unit cost with a lower cumulative production requirement.

So what is leading to the decrease in unit cost for a Tesla vehicle when driving range and vehicle performance are increasing. The key component cost for a Tesla vehicle is the battery pack built with as many as just over 4,400 lithium-ion battery cells for the Model 3 Long Range option using the 2170 cell design. These standard battery cells leverage mature technology produced by multiple well-established manufacturers. Tesla partnered with Panasonic to produce battery cells at the Tesla Gigafactory in Nevada. That reduces the cost for the first unit produced (“a” in the formula) based on this battery cell component.

But at the September 2020 Tesla Battery Day, Tesla announced a new Tesla-designed and manufactured 4860 battery cell design that improves many performance characteristics and a 50% reduction in cost at scale. These 4860 cells have many process efficiency advantages during production and are incorporated directly into the chassis of the vehicle to create a structural battery pack that reduces weight. This is the kind of step change investment required to realize Wright’s Law as cumulative production scales. These batteries will be used initially in vehicles that require more energy density, but eventually as the cost benefits are realized this battery design will likely be used across all Tesla vehicles to improve performance while managing cost to accelerate the transition to sustainable energy.

The 4860 battery cell is a great example of creating operating leverage. The features of this battery help Tesla make their vehicles more desirable with better performance that increases demand. Tesla has reported the cost per kwh for the 4860 battery cell will decrease by 56% at the pack level, but with a 54% increase in energy density and driving range. The key requirements for these gains are the investments and fixed costs to produce the battery at scale. Tesla acquired several companies for key technologies and has made significant investments into research & development on this new battery design. They are still refining the manufacturing process to scale production of the 4860 battery cell. Premium sales of the Tesla Semi, the Long Range 3-motor version of the Cybertruck and Roadster would not be possible without the 4860 high-nickel, no-cobalt, lithium-ion battery cell. The 4860 production currently happens in Fremont, CA in a dedicated Tesla battery innovation factory built to finalize the design and manufacturing process to provide initial commercial production. The 4860 design and production will transfer to Tesla gigafactories when ready to scale. That is disruptive.

The casting of one large Telsa Model Y rear underbody segment is shown in Fig. E3.1-3 to the right. This eliminates separate processes to produce roughly 70 parts that are then spot-welded into a single Tesla Model 3 rear underbody segment shown below to the left. Tesla is also designing a new center chassis segment made with structural cell batteries integrated into its frame to provide even greater efficiencies. The large casted front and rear underbody segments are then combined with this center chassis to form the whole underbody section. Tesla is using the largest casting machines in the world to produce these front and rear underbody segments.

All of this Tesla manufacturing innovation into the “machine that builds the machine” at scale might steepen the rate vehicle unit cost decreases. This further impacts operational leverage and leads to more flexibility. One option is higher gross margins to improve income from operations. The other option is to maintain similar gross margins but use lower unit costs to lower the average sales price to take more market share. Tesla has demonstrated a preference for the latter to accelerate the transition to sustainable energy. That is disruptive.

3. Autonomous Vehicle Navigation

Tesla’s autonomous navigation program combines hardware and software to form a very comprehensive, distributed system to eventually realize a full self-driving vehicle. But training the neural network uses actual autopilot miles driven to build edge cases and exceptions where human driver actions disagree with the neural network. So the pace of innovation is determined by the cumulative autopilot miles (aka driver-assistance supervised by a human driver) driven with the required hardware and software to build reliable data to train the neural network. Tesla delivered approximately 500,000 new vehicles feature-ready with hardware for autonomous navigation in 2020. This effectively doubled the Tesla fleet to about 1,000,000 vehicles collecting edge cases and exceptions to train the neural network across different driving conditions once these outliers are uploaded to Tesla for analysis. The current process requires features to be tagged by human operators, but this process will be automated in the future to accelerate learning using a Tesla-designed “Dojo” supercomputer.

AI scientist Lex Fridman modeled the estimated Tesla autopilot miles driven through January 1, 2021 with just over 5 billion miles driven on all hardware generations. Autopilot miles do not represent all miles driven. For instance, when estimated autopilot miles were 3.3 billion on April 22, 2020, the total estimated miles were 22.5 billion. For comparison, Alphabet’s Waymo reported in early January 2020 their autonomous navigation program had driven 20 million autopilot miles when Tesla had driven about 2 billion (or 100x) on their latest generation 2 & 3 hardware.

Although Wright’s Law has been used primarily to model cost (and time) with cumulative production, we can model cumulative autonomous miles driven as the source of reliable inputs to train the neural network. The output would be the number of vehicle accidents per 100 million miles driven with full self-driving. When this output averages 100 vehicle accidents per 100 million miles driven, reliability would approach 99.9999% or the hallmark of quality known as “6 nines”. Using National Highway Traffic Safety Administration (NHTSA) data in the United States from 2014-2015, there are approximately 800 total vehicle accidents that produce an injury or fatality reported by the police per 100 million miles driven in the US for 16-29 year old drivers. All accidents would actually be higher in these NHTSA data since many accidents do not produce an injury or fatality. And for additional perspective, there were 35,000 highway fatalities reported in 2015 on US roadways with 95% of the automobile accidents associated, at least in part, with driver error. So the opportunity is substantial to improve safety and save lives with autonomous vehicle navigation over human driving that can be influenced by distractions, sleep-deprivation and substances of abuse.

Given the scale of the Tesla’s autonomous vehicle navigation program and increasing automation designed into training the system, Tesla has a significant advantage modeling its progress using outliers (edge cases, exceptions and driver interventions) per 100 million miles driven. These data can be correlated with associated vehicle accidents and fatalities to use more accessible data to predict when 99.9999% reliability is feasible. Tesla has released an updated beta version beyond autopilot called “full self-driving” to a very limited group of about 1,000 Tesla owners. Full level 5 autonomy is expected to be feature ready by the end of 2021, but will require regulatory approval for unsupervised use with or without restrictions.

Regarding operating leverage, each Tesla built and sold hardware feature-ready for full autonomy is being used at limited cost to Tesla to train the neural network with actual driving use in the field. Tesla has made substantial investments into building and operating the neural network, but currently sells the full self-driving service for $10,000 and will soon start selling a monthly subscription for this service to Tesla owners. The neural network needs to know the vehicle model to set some parameters, but will eventually be available across all Telsa vehicles and can be licensed to other vehicle manufacturers, too. This is highly profitable revenue with gross margins likely over 85%.

4. Is Moderna the Tesla of biotech?

Wright’s Law is typically associated with the production of automobiles, airplanes and complex parts, but it has also held up for beer production. Although not specified by Wright, production regardless of the item with a repeatable process for unit production should be in scope with at least 1,000 cumulative units produced. Looking at the pharmaceutical industry, primary input costs include research & development and the regulatory process for commercial manufacturing. Production of the approved product leverages a vast and mature commercial production ecosystem that helps manage cost, but will be different for almost every drug because of differences with each molecule. So Wright is relevant for each drug, but resets with each new drug unless the same drug is produced in higher volumes with additional indications for use.

Biotech companies manufacture larger molecules consisting of biologics like proteins, sugars, nucleic acids and combinations of those. These can be isolated from either humans, animals or microorganisms. The manufacturing processes are usually complex, but an evolving commercial production ecosystem exists. Most biotech drugs require a very elaborate manufacturing, supply chains and packaging processes that also start over with each new unique drug.

However, biotech companies like Moderna, BioNTech, CureVac and Translate Bio have a unique characteristic. These companies manufacture synthetic messenger ribonucleic acid (mRNA) for multiple indications for use. Moderna in particular is focused on producing preventative vaccines and therapeutic mRNA. To do so, Moderna must design an mRNA sequence made up of a very limited alphabet consisting of 4 nucleotide bases: adenine (A), cytosine (C), guanine (G) and uracil (U). This resulting sequence of nucleotides is designed to form a template of triplet codons (e.g. AUG) that hold a code or instruction. These instructions are then used by our cells to translate each triplet codon into its corresponding amino acid (e.g. methionine) to manufacture a specific chain of amino acids into a desired protein. Moderna must also engineer the means to deliver mRNA into cells using lipid nanoparticles (LNP) or an alternative.

Using a non-biological analogy from Moderna’s chief scientific officer of platform research, Melissa Moore, refers to mRNA as Moderna’s iPhone platform. Each unique drug designed is “an app” that leverages this iPhone platform. And just like apps benefit by leveraging the cumulative unit production scale of the iPhone, Moderna is building a repeatable process to print A, C, G, and U. The sequence just changes with each therapeutic mRNA candidate targeting different biological effects. Amgen’s bioreactors that manufacture large molecules are replaced by the recipient’s own body and cells to manufacture a Moderna drug. That is disruptive.

Moderna is also a digital company to exploit the innovation associated with mRNA. The local government of Wuhan, China confirmed in December 2019, that health authorities were treating an unusual type of pneumonia caused by a virus, known now as SARS-CoV-2. The first death was reported on January 11, 2020 in Wuhan. Over the January 11-12, 2020 weekend, Chinese authorities posted the genome sequence of SARS-CoV-2 online for public access. That means biologic samples did not have to be requested and transported by a cold supply chain to Moderna for analysis and to sequence the genome. Moderna downloaded the genome sequence immediately just like downloading a movie on iTunes. They could also start modeling the protein produced by this blueprint. From prior work on coronavirus vaccines, Moderna identified the virus spike protein as the key area of interest to design a preventative vaccine.

Integrating all data and processes allows pre-clinical R&D and manufacturing to share information. Moderna manufactured the first batch of vaccine for SARS-CoV-2 on February 7, 2020. And just 42 days after Moderna downloaded the genome sequence, they sent the first vials of vaccine to the NIH. On March 16, the first inoculation of a human subject took place in Seattle, WA. The speed of this design, manufacturing and quality assurance speaks to both the scientific principles that can be leveraged with mRNA and the digital systems Moderna has put in place. All the capital raised and spent by Moderna to build out infrastructure to scale processes and production for their Moderna COVID-19 Vaccine can be repurposed for subsequent drugs.

Artificial Intelligence (AI) is also a core part of Moderna’s infrastructure for use across most functions. The impact of AI only improves with scale. Moderna is leveraging the COVID-19 Vaccine to build commercial leadership for its mRNA technology. Repeatable complex manufacturing, processes to form core platform technology and digital cloud-services with AI in particular position Moderna more like Tesla than a Pharma company. In Moderna’s case, Wright’s Law applies to the cumulative production of mRNA nucleotide kilo base pairs and the resulting rate of unit cost decline.

Conclusion

Many large global companies use a portion of income from operations to pay dividends and buy back their stock. That is financial innovation found in industries like regulated utilities and consumer staples. But that is not disruptive. That does not win if you are being disrupted by companies like Amazon or Tesla. Forecasting and reliable models like Wright’s Law help estimate the decline in unit costs as unit production scales and are useful tools to estimate market dynamics with a deep understanding of price elasticity for the finished goods. In other words, if I can estimate the roadmap for my cost of goods and target gross margin to establish a narrow range for the average selling price over 3-5 years, I can build the sell side model. If I understand how price influences demand on the buy side then I could estimate the return of accelerating the production to reach lower price sooner if that drives exponential market growth. That is disruptive. Confidence using these tools helps to maintain or accelerate investments into fixed costs that enable disruption when market share and market expansion using operating leverage are key objectives.

A strong corporate vision that addresses very large total addressable markets combined with operating leverage to disrupt those markets over many years is a very compelling story. Tesla is doing this in at least 3 key technological areas tied to electric vehicles with at least a $4 trillion total addressable market (excluding autonomous navigation) if you combine both global vehicles and petrochemicals used to fuel internal combustion engines. The 3 key areas are battery cells, chassis technology/production and autonomous navigation. The operating leverage created by investments in these 3 key technological areas should create substantial income from operations as revenue increases with accelerating demand for electric vehicles. The key results are shown in Fig. E3.1-6 with increasing revenue, gross profit and operating income over 9 years (2012-2020).

The impact of this operating leverage created by Tesla over the last 5 years for electric vehicles should accelerate dramatically over the next 3 years. Once paid subscriptions and sales for autonomous navigation starts to scale, the automotive revenue for Tesla could double with minimal variable cost. The majority of that “incremental” revenue will mostly pass through to income from operations resulting in a much more profitable company than Tesla is today.

And Moderna shares many characteristics when compared to Tesla vs. pharmaceutical and other biotech companies. The digital nature of mRNA research, development, manufacturing and streamlined operations across many drugs provides technological areas to use operating leverage. Moderna is earlier in its commercial journey than Tesla, but the investments made due to the pandemic to produce 1 billion plus doses of the Moderna COVID-19 Vaccine will yield operating leverage for other drugs in the years to come. That is disruptive. For full disclosure, I am an investor in both Tesla and Moderna. I conduct this research as part of my due diligence.

If you are not a subscriber, please consider doing so to get updates on this topic and more.

If you liked this post, please share with your networks so others can benefit, too.

Nothing in this post is intended to serve as financial advice. Do your own research.