[E5] Square: Jack Dorsey's vision for commerce

[E5] Square: Jack Dorsey's vision for commerce

Easy access to financial services for everyone

Dear Reader,

This profile in Product | Strategy | Innovation provides insights into a co-founder and CEO whose company is using an innovation stack to disrupt and transform well-established industries while simultaneously competing with major technology platforms from Alphabet, Amazon and Apple. The bar is high. But the company is making substantial progress executing their strategy. The financial services industry has been dominated for decades by major and regional banks that provide commercial banking services to businesses and financial services to families and individuals.

Square primarily disrupts traditional banking models with low-cost, vertically-integrated Point of Service (POS) systems used by small-to-medium-sized businesses (SMBs). The objective is to make commerce easier for these businesses and their customers. Square uses the POS system and software services to analyze the cash flow within these SMBs. This helps Square determine the risk profile for an SMB and its potential capital needs to grow their business.

Business loan approval is almost immediate and does not require a credit report because Square has more robust and real-time data on the financial viability of the company than any credit service since Square processes the businesses’ payments. Square can also offer paid subscription services to these SMBs to scale their operations using the growth capital provided. As these businesses scale they generate more revenue and need more services.

This enhances the long-term value of these SMBs to Square while the cost to acquire new customers is managed through Seller Ecosystem referrals. It’s a semi-closed ecosystem similar to what Apple has created with their hardware devices & subscription services, but for Square’s SMBs. I use the term semi-closed because Square does provide APIs and a developer network for 3rd party apps to run on the Seller Ecosystem just like Apple enables 3rd party apps to run on an iPhone. But the hardware for SMBs is exclusive to Square.

We will explore the following in this profile after covering the relevant background:

Square is all-in on making commerce easier within a Seller Ecosystem between SMBs and their customers. This disrupts commercial banking.

Square is also scaling a Cash App Ecosystem to provide digital wallet services to consumers in general and the unbanked in particular. This disrupts retail banking.

Square is adopting bitcoin as a “store of value” NOW and a vision for the blockchain future NEXT. This disrupts fiat currencies and cross-border remittance.

Background

Jack Dorsey co-founded Twitter on March 21, 2006 based on his interest in dispatch, microblogging and text-based status messaging. Dorsey served as Twitter’s original CEO for approximately 2 years and navigated 2 successful fund raises to create a novel messaging platform. He was eventually replaced as CEO by co-founder Evan Williams due to Dorsey’s other interests that competed for his time in a fast growing tech startup venture. Dorsey served as Chairman of Twitter after Williams became CEO. Dorsey returned as CEO of Twitter in 2015 and has served in that role ever since.

In the period after being replaced as CEO of Twitter, Dorsey pursued other interests and reconnected with a friend Jim McKelvey in St. Louis where Dorsey grew up. The inspiration for Square came about when McKelvey wasn’t able to complete a $2,000 sale with a customer who wanted to use a credit card. McKelvey operated his glass art business part-time so he did not accept credit cards because of the burden to do so.

Dorsey and McKelvey co-founded Square in February 2009 and initially ran the company out of St. Louis. The Square Reader was the company’s first product launched in 2010 and the product design also inspired the name of the company. The Square Reader was a small square-size device with a 3.5mm audio jack to plug into a smart phone to process credit cards. The user just had to swipe a credit or debit card’s magnetic stripe in the Square Reader to process the transaction using a Square mobile app.

Square’s early Readers had strong encryption and neither credit card numbers, nor magnetic strip data, nor security codes were stored on Square devices to protect personal information. Square continues to invest into its hardware and software technology stack to comply with various standards to compete with the latest point-of-sale (POS) transaction systems.

SMBs have many challenges, but these are only magnified in low-income areas where owner/operators may also have a poor credit history. But bad credit doesn’t limit a winning business idea or viable business with capital needs to grow. Traditional banking just doesn’t service these needs with conventional business models that require credit reports to assess credit worthiness to make business loans.

Low-income communities also have significant challenges for families and individuals who need to access needed financial services like mortgage lending. Investing is also out of reach so two primary wealth building strategies are difficult to access through home ownership and investing in stocks through ETFs or individual holdings. The term unbanked is used to describe the populations in these communities.

Square announced on March 4, 2021 that it was making a $297 million investment to acquire majority ownership in the music platform TIDAL. This is the high-fidelity, artist-owned, global music streaming and entertainment platform that brings fans closer to their favorite artists. TIDAL will operate independently within Square and could form a 3rd ecosystem around artists. TIDAL is a viable platform on its own, but the move to acquire majority ownership could be a negotiating strategy to build a closer partnership with Spotify on better terms.

Square

Company: Square, Inc.

Founded: February 2009, St. Louis, Missouri

Founders: Jack Dorsey, Jim McKelvey, Tristan O’Tierney

CEO: Jack Dorsey

NYSE: SQ

2020 Revenue: $9.5B (+102.1% Year-over-Year)

Monthly Active Users (MAUs): 36 million; Q4 2020 (US, Canada, Australia, Japan, UK, Ireland)

Square’s mission statement is “We believe everyone should be able to participate and thrive in the economy – so we’re building easy tools to empower and enrich everyone.”

Square is a cohesive commerce ecosystem that helps sellers start, run and grow their business. We combine sophisticated software with affordable hardware to enable sellers to turn mobile and computing devices into powerful payment and point-of-sale solutions. Our tools help sellers make informed business decisions through the use of analytics and reporting. Sellers can manage orders, inventory, locations and employees; engage customers and grow their sales; and gain access to business loans.

Our approach is the same with Cash App: we see an opportunity to build a similar ecosystem of services for individuals, providing financial access to all and allowing anyone to send, spend, store and invest money all from one app.

It all aligns with our purpose of economic empowerment – we are helping all kinds of people succeed and grow in the economy.

Benefits for Sellers

The Seller Ecosystem provides easy access to commerce that helps sellers start, run and grow their business.

Start your business. Square turns affordable mobile and computing devices into powerful payment and point-of-sale (POS) solutions to start a business. Software downloaded as mobile apps onto the mobile and computing devices provide the POS services. Businesses can start at no cost using the free Square Reader and mobile app to swipe a customer’s credit card. Square monetizes these solutions with the card transaction fees.

Run your business. Square provides targeted seller solutions for key verticals like restaurants, retail and appointments (used by professional service businesses). Sellers can use analytics and reporting features to make informed decisions about the business. Sellers can manage orders, inventory, locations and employees. Square also offers Team Management and Payroll solutions.

Grow your business. Square provides digital marketing, gift card, loyalty programs and online e-commerce services to help businesses access new customer and sell more to existing customers. Square Capital provides business loans to also help businesses grow.

Benefits for Consumers

The Cash App Ecosystem for individual consumers provides financial access to all and includes 36 million consumers who use Square to send, spend, store and invest money all from one mobile app.

Send. Users benefit from downloading a mobile app to send and receive money with other Cash App users for peer-to-peer (P2P) mobile payments. This can also be used to send cross-border money transfers when users are in countries where Square provides services.

Spend. Users benefit from adding a Cash Card (Visa debit card) for payments and ATM withdrawals. Square provides a rewards program to Cash Card users with discounts called Boosts. Users can use their Cash App account and routing numbers for Bill Pay.

Store. Users can add money by adding a Bank Account and transferring money into Cash App. Users can also enable Direct Deposit so paychecks can go directly into Cash App. Users can create and publish a unique $Cashtag to receive funds by other Cash App users.

Invest. Users can use their Cash App balance to invest as little as $1 in approximately 1,000 individual stocks and ETFs. Selling a stock or ETF deposits funds back into the Cash App balance. Cash App is used to track the investment portfolio. Users can also buy, sell, store, send and receive bitcoin with Cash App.

Product: Mobile Apps: Point of Sale (POS), Dashboard for POS, Restaurants, Retail, Appointments, Team, Payroll, Invoices, Cash App; plus 3rd party Apps from partners like QuickBooks, MailChimp and PostMates; Hardware: Reader for MagStripe, Reader for Contactless (NFC) & Chip, Terminal, Stand, Register, Gift Cards and Cash Card.

Strategy: Target SMBs in key verticals with affordable POS systems to start, run and grow a business. Build a Seller Ecosystem to reduce cost to acquire customers and increase long-term value of customers over time with new services and higher transaction volumes with scale. Attract 3rd party developers to the growing ecosystem. Pay Sellers a generous referral fee to help grow the Seller Ecosystem.

Target consumers with a feature-packed digital wallet to build a Cash App Ecosystem for Individuals. Leverage brands and celebrity influencers to drive adoption with Cash App giveaways direct to their fans on Twitter vs. ads with Facebook and Google to drive awareness.

Monetize these ecosystems with transaction fees, subscription revenue and hardware sales. Fig. E5-3 provides and overview of the 2 ecosystems from the 2021 Square Investor Presentation. These have led to a rapidly growing and profitable base shown in Fig. E5-4 to reinvest income from operations to accelerate growth.

Innovation: Use an Innovation Stack to build ecosystems around Sellers and Cash App for individual consumers. Innovate affordable solutions to democratize access to banking and financial services through Square Capital. Empower anyone with a great idea and determination to start a business regardless of race, gender, ethnicity or socio-economic status. This is highlighted by 2 maps showing Google searches for Cash App and Venmo in Fig. E5-5. The maps are significant because they show as Cash App has scaled, more recent interest is coming from areas with lower socioeconomic status in southeastern US compared the northeast and west coast.

Another innovation is how Square and Twitter partner to reach and scale the Cash App Ecosystem through brands like Burger King and celebrities like Cardi B instead of using ads on Facebook and Google. Twitter is used to broadcast a Cash App giveaway to a celebrity’s fans who reply to the tweet with their $Cashtag. These giveaways have created a viral adoption of Cash App to participate in these giveaways. Square has also partnered with Spotify to build creative ways to engage musicians as influencers and SMBs with merchandise, e-commerce, digital marketing and payroll needs.

If you are not a subscriber to Product | Strategy | Innovation, please consider doing so for updates like this one and more.

1. Square is all-in on making commerce easier within a Seller Ecosystem between SMBs and their customers.

Many businesses large and small transact business with customers at a check-out. This allows selected goods or services to be itemized with the quantity and list price for a sub-total. Sales tax is added for a total price. The customer can then complete the sale with cash, credit card or any form a payment supported by the business. Cash registers have evolved into POS systems to handle multiple payment options.

Square POS hardware spans the no-cost to purchase Reader for MagStripe shown in Fig. E5-1 to swipe credit and debit cards. The $49 Reader for Contactless (NFC) and Chip allows more payments options to be accepted from Apple Pay to cards with a chip. Square charges a transaction fee for each purchase using their hardware.

As POS needs increase, the Square Stand shown in Fig. E5-6 offers a low-cost alternative to more expensive systems. The $169 Stand allows a customer to add an iPad of their choosing and POS Mobile App to complete the system. The Square Terminal is a compact POS all-in-one device that handles MagStripe, Contactless and Chip transactions and print receipts. As POS needs require a Cash Drawer, barcode scanning and printing, the Square Register shown in Fig. E5-2 provides top of the line features for under $1,500.

Square provides Mobile Apps for general POS applications and targeted POS solutions for key verticals like Restaurants, Retail and Appointments (professional service businesses). So, with a $169 Stand, no cost Restaurant Mobile App and iPad, an entrepreneur can add card transactions to a new restaurant without the need for a credit application to process credit cards and regardless of the community.

As a business using Square POS hardware and software scales within a location or with the addition of additional locations, Square sees the scale in real-time through the increase in revenue processed with card transactions. Square Capital can offer business loans or the business can request a loan that is only secured with the cash flow processed by Square.

Entrepreneurs who start, run and grow SMBs using Square hardware, software and services form a Seller Ecosystem. As this ecosystem grows, investment of income from operations back into the ecosystem fuels adding new services to serve the growing needs of these customers. Corporate partners and third party developers are also attracted to business opportunity of the Seller Ecosystem.

Square’s 2021 Investor Presentation describes a Seller Ecosystem with a $100 billion Total Addressable Market (TAM) with less than 3% market penetration by Square. Fig. E5-7 shows the US market alone is an estimated $85 billion TAM with 20 million businesses and $6 trillion in gross receipts. 2.7 million SMBs with gross receipts between $250 thousand to $1 million provide $1.2 trillion in combined gross receipts. However, a mid-market of around 900 thousand businesses with gross receipts over $1 million and up to $100 million have combined gross receipts of $4.3 trillion.

The products and services for the Seller Ecosystem are also shown in more detail in Fig. E5-8. To expand into the mid-market, Square already a robust platform with hardware, software, APIs and services. The mid-market will need more 3rd party developers with solutions already used in those markets, but are ported over to the Square Seller Ecosystem through APIs. More sophisticated lending options from Square Capital will also be needed.

2. Square is also scaling a Cash App Ecosystem to provide digital wallet services to consumers in general and the unbanked in particular.

Easier access to commerce for SMBs is a key need within many communities, but the need for access to financial services for families and individuals is great, too. The US alone provides a transaction volume of $9 trillion spanning sending ($4T), spending ($2T) and investing ($3T). This represents a $60 billion TAM in the US market alone for Square’s Cash App Ecosystem. Square has penetrated less than 2% of this $60B TAM so significant growth is still possible. Cash App was launched by Square in 2013 to compete with PayPal’s venmo, Apple Pay and Google Pay.

The key driver for initial Cash App adoption is typically the need to send or receive money to another Cash App user. This creates an instant deposit by either receiving funds from another user or connecting a checking account to Cash App to send funds. When users add a Cash Card to connect their Cash App balance to transactions with merchants and access Square Boosts to receive discounts with promoted brands, the revenue generated by a user is accelerated with additional use cases beyond sending and receiving money.

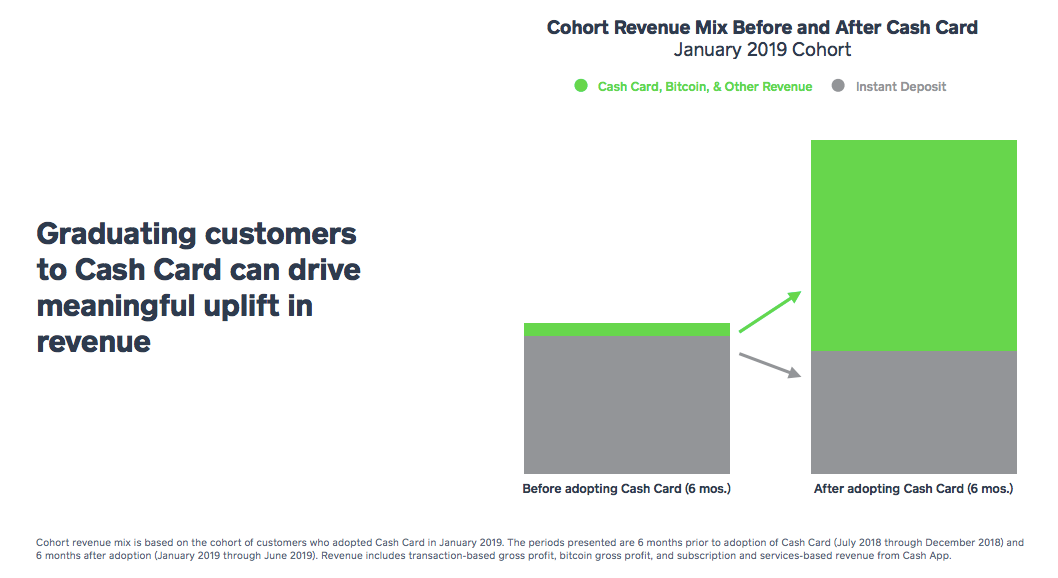

The growth of revenue generated by Square with Cash Card adoption is shown in Fig. E5-9. The analysis selected a January 2019 cohort and tracks revenue for 6 months before Cash Card adoption and 6 months after. The payback period to recover the acquisition cost for new users has also been analyzed with similar cohorts. That payback period is less than 12 months using an analysis on a 2017 cohort and when tracked over 30 months, the return was shown to be $7.7 million on a $1.4 million investment (or +550%).

Direct Deposits are another key driver of revenue since it accelerates the accumulation of funds in Cash App to send, spend, store and invest. Cash App has experienced rapid growth during the pandemic with $377 million in gross profit in Q4 2020 resulting in growth of 162% growth year-over-year. The Cash App customer acquisition cost (CAC) is only $5 as reported in the 2021 Square Investor Presentation, page 27. This CAC is managed using 3rd party brand and celebrity influencers to activate their fanbases with Cash App giveaways.

Investing with Cash App has also become a key driver for revenue. Users can use their Cash App balance to invest as little as $1 in approximately 1,000 individual stocks and ETFs. Selling a stock or ETF deposits funds back into the Cash App balance. Users can also buy, sell, store, send and receive bitcoin with Cash App. Investing puts a key wealth building tool right into the Cash App ecosystem. It allows anyone to adopt the mindset of using a portion of direct deposit to invest in appreciating asset class with an adequate time horizon.

Investing with Cash App has limited features for more advanced investors. It does include trading options, using margin, trading bonds, IRA and other account types and more advanced research tools. Investing with Cash App is for beginning investors. An interesting 3rd party Cash App integration could be using Cash App to build an investment portfolio up to a minimum balance of $10k and then opting in for conversion to a robo-investment tool like WealthFront or discount-broker account with Fidelity. These Cash App integrations could make it more of a long-term fintech and financial services for a growing user base who want a digital wallet.

Leading competitors to Cash App are clearly the PayPal venmo product, Apple Pay, Google Pay and to some extent investing apps from Robinhood and Acorns. A clear differentiator for Cash App is the potential strategic alignment with the Square Seller Ecosystem to unlock benefits transacting with those sellers using Cash App on a contactless Reader.

Strategic partnerships already include Spotify during the pandemic to provide a platform for artists to run fundraising campaigns with their $Cashtag to their fanbases while touring opportunities were basically eliminated. Boost reward partnerships with brands like Chipotle and Subway also demonstrate a path forward to both monetize and drive increasing value for Cash App users with their favorite brands. Twitter also seems to be a key partner going forward to cost effectively raise awareness and drive user adoption of Cash App as previously mentioned.

3. Square is adopting bitcoin as a “store of value” NOW and a vision for the blockchain future NEXT.

Square announced to its Sellers in 2014 that they could start accepting bitcoin as a form of payment in the Square Market for their online stores. Any business in the Square Seller Ecosystem can create a free online store in the Square Market.

Square expanded available services for bitcoin by launching a feature in 2018 to Cash App users (in all but 4 states) to buy, sell, store, send & receive bitcoin. This generated a lot of interest in Cash App because trading bitcoin could be done directly without an exchange like Coinbase. Venmo has also added this bitcoin capability to its platform.

Square further expanded adoption of bitcoin with the announcement of the purchase of $50 million in bitcoin with its corporate cash or approximately 1% of total assets on October 8, 2020. This trend has included other companies like MicroStrategy and Tesla as a hedge against holding large sums of cash. During the 4th quarter earnings call on February 23, 2021, Square announced they had purchased another $170 million in bitcoin as of December 31, 2020 representing 5% of total assets.

The adoption of services to buy and store bitcoin for Cash App users and Square itself supports the use case of bitcoin as a “store of value” similar to a digital gold asset. However, using an asset in this way is speculating that it will be worth more later or hold its value better against a fiat currency or currencies during an event like hyperinflation.

But what is Square’s long-term vision for bitcoin. Simply stated Square aims to make bitcoin the planet’s preferred currency. Or bitcoin as the best money. Square is adding additional bitcoin services for its Cash App users like cold wallet storage with Subzero to hold bitcoin assets offline in an open-source hardware security module (HSM). More details on Subzero are available on GitHub. An offline cold wallet reduces the risk of a remote attack.

However, Square has an even bolder vision for bitcoin and cryptocurrencies in general supported by the creation of the non-profit open-source organization Square Crypto to advance the use of cryptocurrencies and blockchain technology through internal projects like the “lightning development kit” and organization grants to support external projects like “The Eye of Satoshi” that monitors bitcoin transactions for malicious activity. Square CEO Jack Dorsey also supports bitcoin projects like funding a blind irrevocable trust with music artist and businessman Jay-Z in the following tweet.

And looking at blockchain technology and non-fungible tokens (NFTs), Square can leverage smart contracts on the Etherium network to help monetize art in many creative ways. Square’s acquisition of majority ownership in Jay-Z’s TIDAL platform for artists earlier this year provides a vehicle for Square to do for artists what it has done already for SMBs (with POS services) and consumers (with the Cash App). Creating an online presence for artists to sell merchandise is straightforward, but leveraging Square’s blockchain initiatives could provide an entirely new way for artists to monetize their core work or side interests.

The artist Grimes combines her interests in music and digital art to create a whole platform around her brand. She recently used NFTs to fund a project around one of her digital art collaborations that sold for $6 million earlier this year. Square + TIDAL can become the scalable platform for artists to engage their fanbases in new and creative ways including high-fidelity music streaming to fund their work and make a viable career out of music and other media for more artists.

If Square + TIDAL helps create the vision for a more digital and blockchain-enabled future for artists, then Spotify can also partner with its global scale to bring even more capital, artists and fans to that opportunity. Square and Spotify have already partnered on some creative initiatives to help artists during the pandemic.

Conclusion

Banking and financial services are needed by any business, family or individual. Yet justice is not served with private banks only serving the wealthy and commercial banks biased towards larger corporations. And retail banks serve businesses, families and individuals predominantly in middle-to-high income communities. Banks do serve lower income communities, but fees may be higher and with more burdens to qualify for services. So many in these lower income communities remain unbanked.

Square levels the playing field as a fintech innovator using digital scale to provide free and easy access to key services for businesses, families and individuals. Fig. E5-9 shows free access to engage a platform works. Just as Nucor disrupted the steel industry with just-in-time steel manufacturing starting with low margin rebar that the incumbents were willing to give up, Square is adopted by businesses and consumers that are ignored by major banks or unbanked.

But that is not the end game. In the 2021 Square Investor Presentation, the company presents the opportunity to go up market into the mid market that is 3.5x the SMB market. Just like Nucor went up market from low-margin rebar, Square will take market share in the mid market and eventually the Enterprise market to compete directly with the big Banks.

If Square continues to execute and successfully moves up market, it will not just disrupt big and regional banks, but will likely destroy the weak ones. Nucor was discounted as inferior until it competed head-to-head with US Steel and other incumbents for high-margin steel products. Strategic partnerships will likely determine how far upmarket Square disrupts. A big bank could leverage Square to accelerate a social justice agenda and to cost effectively access new customers. A discount broker could access new customers through Cash App investors.

But what is really compelling about Square is the rapid growth of their consumer Cash App ecosystem. As that ecosystem scales from 36 million users primarily in the United States to something like the 345 million global Spotify users [E4], Square becomes a strategic partner for the $6.2 trillion Enterprise business market whether they adopt Square POS systems or not.

Just as Nucor disrupted big steel, Square will disrupt big banks and bring more justice to banking and financial services along the way. We need more “Squares” in every industry. And all of this thanks to a visionary founder, owner & operator who had a fascination with dispatch. Kudos to Jack Dorsey. An equalizer and capitalist at the same time.

For full-disclosure, I follow Square with a primary interest in their products, strategies and innovation, but as a retail investor, I’m also long SQ and SPOT mentioned in this profile.

Best,

Stephen

If you are not a subscriber, please consider doing so to get updates on this topic and more.

If you liked this post, please share with your networks so others can benefit, too.

Nothing in this post is intended to serve as financial advice. Do your own research.