[U33] Block: corporate strategy translated into a meta-ecosystem

[U33] Block: corporate strategy translated into a meta-ecosystem

A fintech disrupting traditional financial services with an ecosystem of ecosystems

Dear Reader,

For this Update in Product | Strategy | Innovation I will explore the expanded corporate strategy of a major fintech company focused on 4 ecosystems spanning consumers, sellers, creators and Bitcoin with $16.5 billion in revenue over the trailing twelve months. Block (NYSE: SQ; formerly known as Square) recently held its 2022 Investor Day to discuss all the changes since a similar event 5 years ago. A link to a video of the entire 5+ hour event is provided at the end of this update with time stamps to key segments. The video segment on the Block Business Model by CFO, Amrita Ahuja is particularly insightful and starts at time stamp 4:04:05.

Square

Square launched its first product in 2010 with a simple hardware device and mobile app so small business owners could close more sales using their mobile device to process credit cards. Early adopters were often street vendors and food truck operators who were losing sales because they could not accept credit cards. In many cases, these were entrepreneurs who ran good businesses, but were underserved by traditional banks due to poor credit. Square focused on the unmet needs for these business owners and kept innovating solutions.

Today, the Square business provides a full stack of integrated software, hardware and financial services for small-to-medium-sized businesses with $250k-$1M in annual gross receipts and mid-market businesses with $1M-$20M & $20M-$100M in annual gross receipts. Enterprises with over $100M in annual gross receipts are an emerging segment for Square. Yet, even with all of Square’s success over the last 12 years, it has only penetrated 4% of the small-to-medium-sized business opportunity and less than 0.5% of the mid-market business opportunity.

But one of the key attributes that makes Square so compelling is it can just as easily serve micro-market businesses with under $250k in annual gross receipts. There are over 17 million of these businesses in the U.S. and these businesses are the source of future small-to-medium-sized and mid-market businesses. Square has penetrated 13% of micro-market business opportunity to-date. Square’s role as a catalyst to accelerate growth for these micro-market businesses will evolve as it scales products and services across all sizes of businesses.

Cash App

Square’s team launched Cash App (formerly Square Cash) in 2013 to expand serving unmet needs from businesses to consumers. Many Cash App early adopters were unbanked consumers in areas where banks were not readily available or easy to access. The adoption of Cash App usually starts with sending or receiving cash among friends and family, but for the unbanked, use soon evolves to include direct deposit of paychecks. Users can add a Cash App Card to pay for goods and services and withdraw cash with an ATM.

Today Cash App users can also trade and hold stocks, ETFs and Bitcoin in addition to cash through the same app using its digital wallet feature. Cash App allows users to borrow based on their inflow and outflow history. Bitcoin accumulated and self-custodied through a Cash App account could also be used as collateral for bigger loans to start a business that could leverage Square services. Services to file taxes for consumers are also available after the acquisition of that business from Credit Karma.

TIDAL

Out of Square’s executive and small business focused teams, it determined music artists and other creators have many of the same business needs as other small business owners who were currently served by Square’s tools and services. In 2021, Square acquired majority ownership of TIDAL, the global music streaming platform owned by musician and entrepreneur Jay-Z. TIDAL includes both free and paid subscriptions, but differentiates its service from Spotify and other streaming services with high fidelity sound and programs to support artists.

Music artists accelerated Cash App adoption as key influencers with promotions offered to their fans. Cash App Studios was launched in 2021 to bankroll emerging musicians and other artists. Cash App is used to facilitate payments from fans, Square is used for banking, and recorded music can be released on TIDAL.

However, I think the ultimate vision for TIDAL is not to take on mainstream music streaming services like Spotify, Apple Music, Amazon Music and others, but to disrupt the recording labels who take as much as 50% of the revenue generated by a musician to distribute and promote their work. But this new business model needs to develop early with artists before they sign with a record label. As TIDAL scales with emerging artists, it becomes more strategic to the mainstream streaming services. Top artists could leave recording labels to join TIDAL under a new brand as an independent artist and negotiate better streaming terms with services like Spotify.

Block and Bitcoin

Block was formed in November 2021 as the parent company of Square and its peer businesses Cash App and TIDAL plus a series of initiatives around Bitcoin. A non-profit initiative started as Square Crypto to help advance Bitcoin was renamed Spiral under Block. TBD was announced to build the decentralized infrastructure needed to empower more people to participate in the global economy. And hardware is also being developed to support programs for Bitcoin mining and more mainstream cold wallets to self-custody Bitcoin.

So Block is the brand and vision for an entire Ecosystem spanning multiple ecosystems that include:

Square ecosystem

Cash App ecosystem

TIDAL ecosystem

Bitcoin ecosystem

The strategy is each ecosystem focuses on a key vertical or related verticals like Restaurants, Retailers, and Service businesses for Square to focus on their unmet needs to drive value through hardware, software and financial services. Additionally, as these ecosystems scale, Block aims to create additional value across these ecosystems. For instance, the Cash App ecosystem can benefit from loyalty programs run by the Square ecosystem. And the Cash App, Square and TIDAL ecosystems can eventually leverage the Bitcoin ecosystem to rely less on Visa, Mastercard and traditional banking networks.

Block acquired Afterpay in an all-stock transaction closed in January 2022 to connect the Cash App and Square ecosystems with buy now, pay later services used around the world by millions of consumers and businesses of all sizes. This acquisition accelerates the penetration of Square services within mid-market and enterprise businesses and adds a valuable service to Cash App users who buy goods and services through these businesses. Square also offers access to Afterpay for small-to-medium-sized businesses to close more sales.

3 Key insights into Block’s future

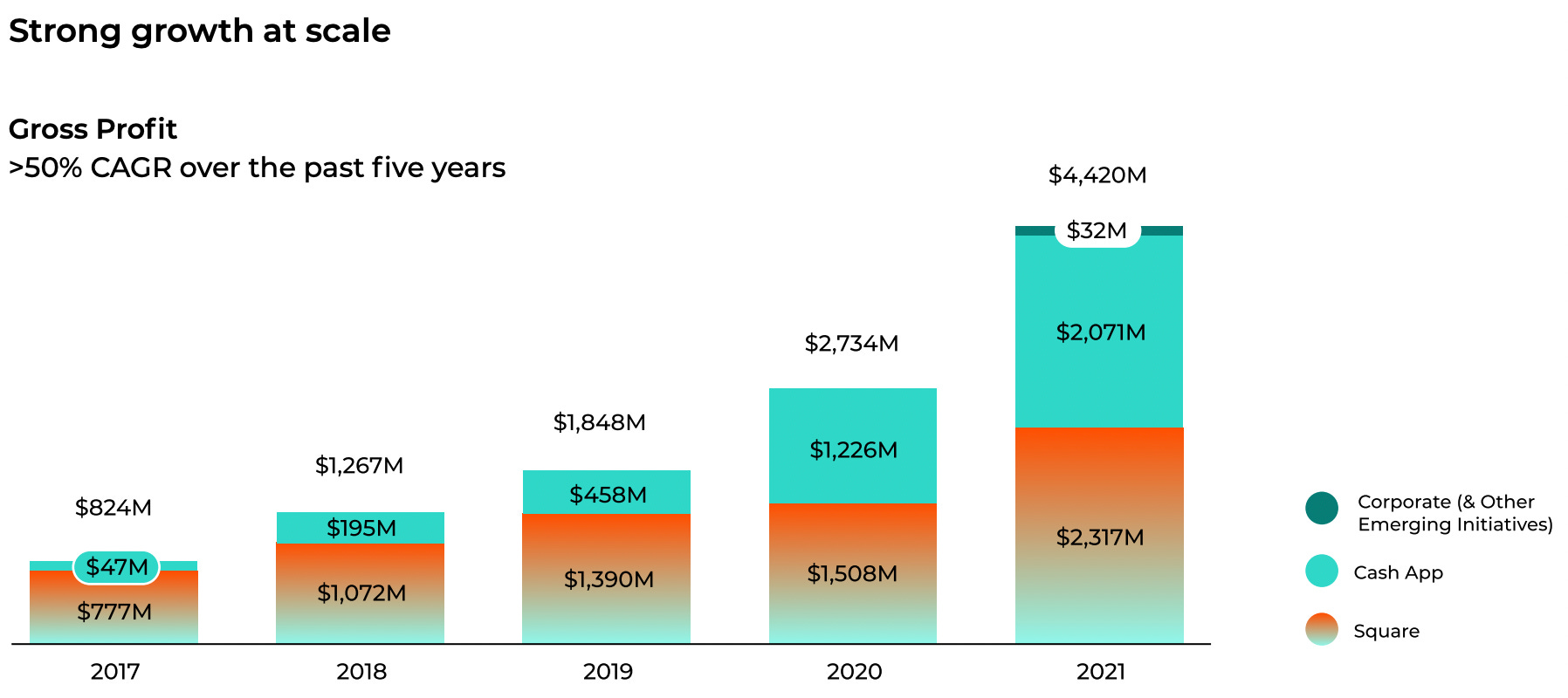

Block provided a corporate strategy and business model update with its recent 2022 Investor Day on May 18. One of the key talking points on Block’s corporate strategy was moving from a focus limited to the Square and Cash App ecosystems to a more comprehensive Ecosystem of ecosystems strategy. This evolution in strategy is an outcome of several significant corporate acquisitions and the expansion of corporate initiatives to create new ecosystems and to build strategic connected services across these ecosystems. I left this Investor Day with 3 main takeaways related to product, strategy and innovation going forward to build on strong growth in gross profit over the last 5 years illustrated with the following graphic.

1. Patience, efficiency and continuous innovation are key to win a large global market like financial services.

Block provided more insight into its business model and expanded $190 billion serviceable addressable market (SAM) with existing products and services in its current markets. This SAM is relative to the estimated $28 trillion total addressable market (TAM) for global financial services by 2025.

The growth potential for Block is substantial, but even more so in a scenario where the US dollar, China renminbi and Bitcoin consolidate global markets. Ant Group and Tencent control market share in Asian markets, but Block is positioned to compete for the rest of the global financial services market against Visa, Mastercard, Paypal, Stripe, Fiserve, and Ayden and eventually global banks like Mitsubishi, JP Morgan Chase, HSBC, BNP, Bank of America and Wells Fargo.

Block’s cost to acquire a customer for Cash App is $10 compared to $300-600 for retail banks and $30-50 for internet-only neobanks. And the gross profit per monthly active user (MAU) has grown from $5 in Q4 2016 to $47 in Q4 2021 with continuous product launches to serve the growing base of 80 million annual active Cash App users. Cash App’s ROI related to customer acquisition over a 3 year period is greater than 600%.

But the key business model for the Cash App ecosystem going forward is (MAUs) x (inflows per active user) x (monetization rate) across key products like peer-to-peer transactions, stock trading, Cash App Card, taxes, borrowing and direct deposit. Future drivers to further enhance the monetization of inflows per active user will include more Bitcoin related features and Cash App Pay linked to Afterpay and commerce with Square sellers. Cash App is also a candidate to become a super app like Tencent’s WeChat where a single app consolidates more services with tabs vs. a single dashboard used by multiple apps.

The Square ecosystem strategy has expanded to focus on omnichannel software so sellers of all sizes can close more sales in person, over the phone, on the web, and across social/chat channels. Gross profit with omnichannel has grown 600% since 2017 and in 2021 represented 49% of total gross profit for Square at $900 million. Square is also expanding globally with France and Ireland added in 2021 and Spain in 2022 to the United States 2010, Canada and Japan 2012, Australia 2016, UK 2017 and Falkland Islands (UK) 2020. The Afterpay acquisition is expected to accelerate this global expansion with strong demand for buy now, pay later services.

Square is prioritizing expanding customer acquisition upmarket with larger sellers across its key verticals spanning restaurants, retailers and service businesses. Square has grown gross profit 19x since 2015 across businesses with over $500k in annual gross profit. And larger sellers use more software products and services. Upmarket expansion is also accelerating with the Afterpay acquisition because this is a popular feature to close more sales even at major retailers.

2. Underserved and unbanked small businesses, consumers and creators are fundamental to Block helping more people access the economy.

Square has focused from day 1 on helping more business owners close more sales. Square did not require these business owners to complete a credit report because they could deduct fees directly from sales tied to credit card transactions and limit outflows until transactions cleared. However, many businesses using Square would start using their Square account just like a bank account and accumulate a cash balance.

Square eventually started extending capital to businesses that were growing positive cash flow to help accelerate growth. Square had the business intelligence into daily transactions to risk capital with thriving businesses. This small business demographic was ignored by traditional retail banks, but is profitable for Square.

When Cash App launched, early adopters were also the underserved and unbanked. But Cash App could limit its risk through cost efficient peer-to-peer cash transfers that led to more inflows through direct deposits. But the lower costs to operate Cash App and its viral growth allowed this ignored consumer demographic to be serviced with Cash App.

And borrowing with Cash App is much more cost effective for consumers than “payday loans”. Cash App is popular with teens to build financial intelligence managing money under the supervision of their parents. Cash App can later be used like a bank during college and early in a career to transfer funds, accept direct deposits and pay bills. Spare cash can be invested into stocks, ETFs or Bitcoin.

TIDAL and Cash App Studios are dedicated to fostering creators with a focus on emerging music artists. Linking Square and Cash App services with TIDAL music distribution provides the business intelligence similar to Square to risk capital on emerging artists who are building traction with their fans.

If TIDAL scales with emerging artists, more established artists could also switch to TIDAL to build their own businesses as a creator entrepreneur versus using a recording label to distribute and promote their work. TIDAL can reward fans using Cash App to promote their favorite artists.

And easy access to Bitcoin and open-source source tools to build fintech applications using the Bitcoin payment network empowers more consumers, businesses, creators and software developers to participate in the economy. Decentralizing financial services is a core Block objective to make these services more inclusive.

3. Cross-Pillar value drivers can build a dominant global financial services Ecosystem

The vision of Block is to build vertically-integrated, independent ecosystems focused on consumers, sellers, creators and Bitcoin. But creators are really just another seller vertical that can leverage core and new products and services across Square, Cash App and Bitcoin.

I’m sure Block wants to create something unique with its vision, but I gain confidence in Block’s strategy when I reduce their 4 ecosystems into 3 Pillars spanning consumers, businesses and Bitcoin services. This is basically the Amazon 3-Pillar strategy with Prime, Marketplace and AWS repurposed for financial services. The biggest unknown is whether Block’s strategy for a Bitcoin payment network can scale to anything like AWS has for cloud computing.

Amazon has mastered taking an expense like an IT department and turning it into the hugely profitable AWS Pillar that sells the same services it uses internally across its other 2 Pillars to other companies. Block is also motivated to save credit card transaction fees paid to Visa, Mastercard, American Express and Discover; cross-border transaction fees and corporate treasury costs. Block plans to build software services on top of the Bitcoin payment network to disrupt all conventional payment networks. Block will primarily use these financial services to drive value for customers across its Cash App and Square Pillars.

And like Amazon uses its Prime Pillar to offset its customer acquisition cost and enhance the long term value of a customer through paid subscriptions, Block has Cash App to offer value direct to 80 million annual active consumers and growing. Cash App is a top 10 app in the app stores and has ranked the #1 financial services app over the last 5 years. Amazon Prime has penetrated more US households with 150 million users, but Cash App has no barrier limiting the same penetration with an app that is free to download and start using at no cost for peer-to-peer money transfers.

Block saw a major value driver for both Cash App and Square users with buy now, pay later services popular among younger users. Block acquired Afterpay in an all-stock transaction valued at $29 billion earlier in 2021 and made the Afterpay features available immediately after the acquisition closed to all Square sellers in the US and Australia.

Cash App is integrating a Pay feature into its app to offer buy now, pay later to its own users. The objective is to close more sales between Cash App buyers and Square sellers with benefits provided to both participants in the transaction over traditional credit cards. Cash App Boosts and Square loyalty programs can further incentivize the synergies and value created between these 2 Pillars.

Conclusion

Block aspires to play a major role as a fintech leader in the global financial services market. Block is also disciplined to efficiently deploy capital towards continuous innovation and customer acquisition. This will accelerate with the Afterpay acquisition for 2 main reasons. First, Afterpay allows Square to scale upmarket with larger sellers including enterprise retailers who typically deploy more Square services than small-to-medium-sized businesses. Second, Afterpay allows Cash App and Square to cross-sell services to drive more value for their customers. Omnichannel software will also be a key strategy to scale Square.

Block can further capitalize on Afterpay by realizing the “alpha” payment network built on top of the decentralized Bitcoin blockchain. Block will continue to build out the base infrastructure as an open-source initiative for other companies and developers to contribute and use for their own work. This will drive additional value for Cash App and Square customers beyond “buy now, pay later” and disrupt traditional credit card payment networks. This should be a winning strategy whether it takes 10, 20 or 30 years. All Block really needs is adequate time to execute. And Bitcoin would become more than just a speculative store of value if it provides the base layer to settle transactions on such a scalable payment network.

If Block is successful creating this Ecosystem across 3 core Pillars as Amazon has done over the last decade, Block could become one of the largest global corporations. Block products and services could impact billions of people around the world and move trillions of dollars annually to expand local, regional, national and global economies. I’m not sure if that is what Jack Dorsey intended when he co-founded Square. He likely just wanted to help more businesses close more sales to create his next venture after Twitter.

Best,

Stephen

I’m long SQ and SPOT mentioned in this update. Nothing in this post is intended to serve as financial advice. Do your own research.

6:14 Opening and legal disclaimer

9:01 Our Ecosystem

17:43 Market Opportunity

55:16 Square Ecosystem

1:41:00 Cash App Ecosystem

2:41:46 Afterpay: Connecting Cash App and Square Ecosystems

3:15:08 TIDAL

3:28:18 Bitcoin Ecosystem

4:04:05 Business Model

4:44:14 Q&A Session (edited)