[U40] Lemonade: can we innovate insurance?

Transforming a necessary burden into a social good

In the last Update, I reviewed 2025 Objectives for the fintech company Block. This company is building products and services to advance global financial services. Block’s technology goes beyond just processing transactions to learning about the financial fitness of its customers. And then working with these customers to improve key functions within their operations to help fuel growth.

Sentiment soured towards growth-oriented companies in 2022. Many tech companies have announced layoffs and cost controls are more common. This trend will likely continue until there is more certainty around when interest rates are expected to settle into more sustainable levels. But meaningful innovation during such times can also accelerate growth as market conditions improve. Block was founded during the financial crisis in February 2009.

In this Update for Product | Strategy | Innovation I will discuss a company reimagining insurance within the broader financial services industry. The company was founded just over 7 years ago, but has experienced significant growth with annual premiums reaching $609 million in the Q3 2022 quarter with 76% year-over-year growth.

The company is Lemonade and is also experiencing substantial losses with $234 million in net losses year-to-date in the same Q3 2022 quarter end. Artificial intelligence to manage risk and a new business model are fundamental to Lemonade. Success depends on machines learning faster than consuming invested capital to achieve sustainable growth. This is more critical than ever in the current interest rate environment with such negative sentiment towards companies generating substantial losses.

Background

The global insurance sector is estimated to reach over US$6 trillion by 2025 and provides a key segment within the financial services industry. The basic concept of insurance is one party, the insurer, will guarantee payment for an uncertain future event. The other party, the insured or policy holder, pays a smaller premium to the insurer in exchange for the protection on the uncertain future event.

Evidence of businesses distributing risk dates back to 1750 B.C. in Babylonia within the Code of Hammurabi. The insurance industry has evolved over many centuries with multiple ownership structures, business models and insurance products used today. Ownership is usually by stockholders with equity in an insurance company, but mutual insurance companies are owned by its policyholders. Profits by a mutual insurance company are either retained in the company or returned to policyholders in the form of a distributed dividend or reduced future premiums.

Legacy insurance companies have the benefit of developing abundant claims history using many policies and customers over many years of business. Actuarial science uses these data plus mathematics, probability and statistics to quantify risk. Insurance has also matured over the years with many different stakeholders providing an insurance value chain that can span:

product development,

marketing,

sales & distribution,

new business underwriting & risk management,

policy administration & servicing,

claims management, and

finance & accounting.

This allows specialization with specific core competencies and sourcing the rest to complete the value chain. This also creates certain efficiencies with scale, but encourages a focus on specific products, customers and policy attributes. It can also incentivize profit at the expense of policyholders.

Legacy insurance has provided opportunities for the capital markets to generate attractive returns on invested capital. Warren Buffett and Berkshire Hathaway have used GEICO auto insurance, reinsurance and other insurance business lines to generate substantial returns over many decades.

Publicly-traded insurance companies like UnitedHealth Group, Chubb, and MetLife can also generate income for investors through paid dividends. But legacy insurance typically represents low-beta value vs. high-beta growth for shareholders.

Direct-to-Consumer “Insurance Technology” Companies

An emerging trend is the emergence of growth-oriented insurance technology (insurtech) companies. Boston-based Insurify simplifies sourcing auto, home and life insurance online for consumers and acts as a cost-effective channel for legacy insurance carriers to acquire new business.

Oscar Health offers health insurance with a full technology stack to quote policies, process claims and provide other services. Oscar offers Medicare Advantage plans; health insurance for individuals, families and businesses; and health insurance for small businesses through a partnership with Cigna.

Insurtech companies can focus on innovation and partner with a reinsurance company to insure risk for a specific product. This reduces the regulatory and financial requirement to validate a new product or business model. Sales & distribution can also be sourced through third parties.

Companies that vertically integrate the insurance value chain as a full-stack carrier are heavily regulated and require a license in every state where they operate plus a federal license, too. Underwriting risk requires adequate reserves on the balance sheet to pay claims. Reinsurance can be used to offset as much of this risk as needed to support the available capital structure.

Lemonade, technology plus a new business model for Insurance

The insurtech company Lemonade (NYSE: LMND) was founded in 2015 to reimagine every aspect of insurance as a full-stack carrier. A founding principle was to build trust with customers using behavioral economics. Lemonade uses a fixed 25% fee from an issued policy to cover administrative expenses and profit. The remaining 75% is used to insure risk and pay claims.

Any surplus for a customer cohort at the end of the year is paid as a Lemonade Giveback to a non-profit cause selected by that customer cohort. Lemonade has partnered with over 100 causes to enable the Giveback program. This incentivizes cost reduction by both Lemonade and its customers. It also intends to reduce customers filing frivolous claims. For all these reasons, Lemonade sells its insurance products, processes claims and services accounts direct with customers using digital and mobile-first tools.

Lemonade designed and implemented its own information technology infrastructure to support artificial intelligence and machine learning development. This helps define the right customer attributes for each product, price insurance policies, enhance the customer experience and reduce losses over time. Lemonade can then train its internal systems by acquiring customers and issuing policies. It can quantify risk for each customer and then compare payments received against claims paid.

Lemonade is a publicly-held, for-profit, benefit corporation and certified B Corp. This business structure helps balance social impact for stakeholders along with profits for shareholders. This creates the need to balance the number of supported causes with the growing give-back dollars.

Lemonade’s strategy spans 3 key areas of focus to drive sustainable growth.

Drive Healthy Growth - Do we have the right products, pricing & bundling?

Manage Expense Ratio - Do we have the right processes and automation to reduce our costs to acquire customers and provide superior customer experiences & support?

Manage Loss Ratio - Do we have the right processes and automation to manage risk?

Lemonade uses machine learning to improve outcomes associated with each of the 3 areas of focus above. One key objective is to improve profitability using the Long-Term Value (LTV) of a Customer divided by the Cost to Acquire a Customer (CAC). An ideal target for LTV/CAC is 6.0 or greater to help drive profitable growth with invested capital. However, Lemonade’s longest running insurance product for Renters was reported to have an LTV/CAC of 3.2 in Q3 2022 with 1.4 million customers. Profitability was even lower with Lemonade insurance for Homeowners in Q3 2022 with an LTV/CAC of 1.6. This is one of Lemonade’s biggest challenges. They have shown they can grow new customers, insurance products and premium revenue, but can they sustain their growth.

The Loss Ratio is not really sustainable long-term for product lines other than Renters insurance (loss ratio estimated at 55% in Q4 2022 ) whereas Home insurance is estimated at 117% and Pet insurance is estimated at 86%. The Loss Ratio drives the 75% cash outflow target from premium revenue. Lemonade’s Base case for profitability by mid-2026 assumes 20% premium revenue compounded annual growth, 70% loss ratio across all insurance products and 25% of customers carry multiple insurance products to improve the LTV for a customer. The U.S. property and casualty insurance industry average loss ratio was 71% in 2019.

Artificial Intelligence (AI), Machine Learning (ML) and Neural Networks

Microsoft, Alphabet, Amazon, NVIDIA, Tesla and Palantir are technology companies usually associated with AI & ML. Lemonade can access the tools from these companies to build out its insuretech platform for the insurance industry. But what prevents legacy insurance companies from using this same playbook.

Lemonade would argue they are not just about technology but the combination of actuarial science, machine learning, direct-to-consumer services and behavioral economics. This playbook is harder for legacy insurance companies to replicate. This is also a key benefit of vertical integration where machine learning is optimized with the full-stack of data across an entire value chain.

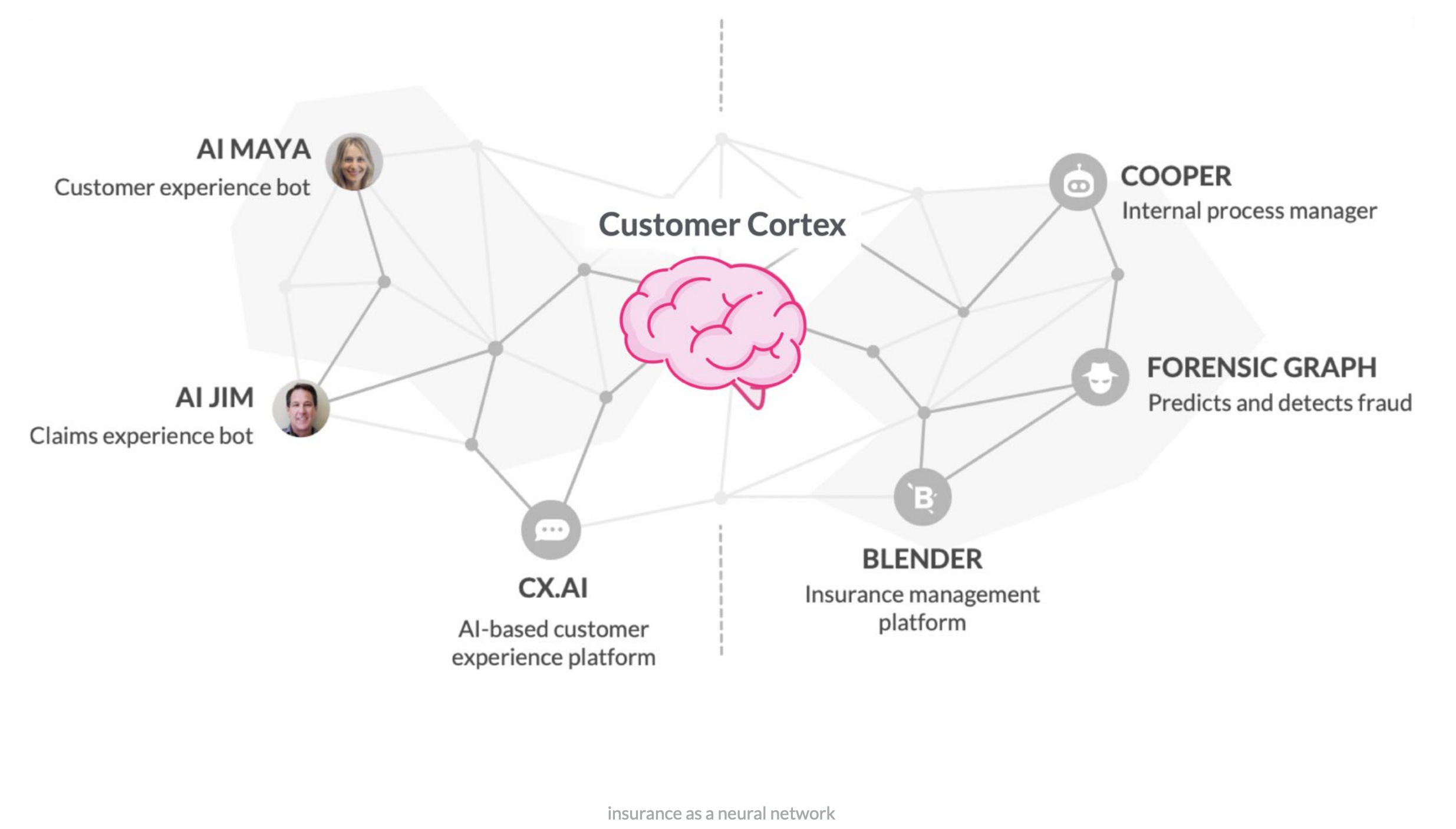

Lemonade’s Machine Learning model

The neural network Lemonade is building and improving with real-time use in the market can price and issue policies and monitor loss against claims. Lemonade stated at their 2022 Investor Day, they have used 100s of millions of customer interactions with 160 terabytes of textured data to train about 50 machine learning models.

COOPER monitors servers, handles tasks, deploys virtual environments and pushes over 12,000 builds into production annually. This also saves 10,000 hours of human software development hours a year and helps control the expense ratio.

The AI MAYA customer experience bot automates selling 98% of Lemonade’s insurance policies versus legacy insurance companies that sell 95% of their policies with a human. This human element costs 15% of premiums in perpetuity. This automation with AI MAYA also helps Lemonade control its expense ratio.

The CX.AI customer experience platform handles 1/3 of all customer requests like adding a spouse, changing an address, and much more. This also helps manage the expense ratio.

AI JIM takes first notice of loss (FNOL) for 98% of claims, and handles 45% of claims end-to-end, with a level of accuracy that surpasses humans. This helps manage the loss ratio.

Fraud algorithms flagged over $100 million in fraudulent claims, and detected doctored documents in $12 million worth of claims. This also helps manage the loss ratio.

Watchtower tracks wildfires and weather, automatically halting marketing, and instituting a delayed-start-date for affected areas. This also helps manage the loss ratio.

Computer vision and Natural Language Processing (NLP) using satellite images detect risky homes for underwriting review, with a hit rate of ~80%. This also helps manage the loss ratio.

Partnerships

Access to key customers and reducing customer acquisition costs are key priorities for Lemonade to manage its administrative costs. That is why cross-selling multiple lines of insurance to existing customers is so important.

Access to new customers is also possible through strategic partnerships. One example is a new partnership announced for 2023 with Chewy to promote Lemonade pet insurance to Chewy customers who buy food, medications and other supplies for their pets online. Over 80 million households in the US have pets, but only 2.5% of those households have pet insurance. The US pet insurance market was estimated at $2.6 billion in 2021 with 25% annual growth.

Lemonade acquired Metromile to accelerate entering auto insurance with over $100 million in-force premiums, 49 state licenses in the US and telematic data on miles driven to model auto risk and to price insurance by the mile. This also allows Lemonade to bundle and cross-sell other insurance products to Metromile customers.

Millennials are the largest customer demographic for Lemonade. This is a key group because if Lemonade can win over a millennial with low-cost renters insurance and grow premium revenue as more lines of insurance are added over the life of such a customer, this is a very efficient strategy to reduce the customer acquisition cost. The original cost is leveraged across multiple insurance policies with no incremental customer acquisition cost.

Millennials are a key age demographic for fintech company Block among its 49 million monthly Cash App transacting users as of September 2022. Cash App partners with musicians and celebrities to reach the millennial demographic with promotions to their fan base. This offers unique partnership opportunities for Lemonade and Cash App to consolidate the primary financial services used by these young adults with renters and auto insurance, banking, direct deposit, and investing.

Amazon Prime’s 150 million customers in the US would offer access to key customer demographics. Fintech company Affirm partnered with Amazon to offer the Buy Now, Pay Later feature to Amazon customers making online purchases for more expensive items. This may require a unique partnership model for Lemonade and Amazon to co-develop proprietary models for a specific business line using the combined machine learning resources of both companies. Amazon can also host cloud data and provide routine cloud services. The terms may not be acceptable to make this option reasonable.

Tesla as a strategic partner would offer customers to Lemonade with higher disposable income and the opportunity to bundle Tesla’s auto insurance and telematics with other lines of insurance. This may also require a unique partnership for Lemonade and Tesla to co-develop proprietary models for auto insurance and to make Tesla auto insurance more competitive by bundling with other insurance products from Lemonade. Tesla EVs can also be a key component to reduce the loss ratio for auto insurance as safety continues to improve.

Lemonade itself could also be a strategic insurtech partner for a holding company like Berkshire Hathaway and it’s group of legacy insurance companies. Berkshire Hathaway could lower its costs to operate its insurance companies with more process automation. However, Lemonade might prefer to only access working capital to improve its own internal processes for Lemonade customers.

Conclusion

Lemonade is a young insurtech company within the $6 trillion global insurance industry. They started with low-cost renters insurance, process automation to save costs and a business model focused on behavioral economics to build customer loyalty and reduce fraudulent claims. Lemonade is growing insurance premium revenue like a tech company, but their losses are substantial while they improve their pricing and risk management models. The cost of maintaining these losses will only increase with higher interest rates.

However, the vertical integration and process automation Lemonade is building to source, price and issue insurance policies as well as manage claims could add significant operating leverage as Lemonade scales. Strategic partnerships like the one with Chewy as the leading online pet supply marketplace, helps lower customer acquisition costs for target customer profiles to offer pet insurance. Lemonade can then cross-sell and bundle other lines of insurance to further reduce customer acquisition costs.

Depending on the macroeconomics that develop over 2023 and 2024, Lemonade may need a strategic partner in the insurance industry to leverage resources and working capital to help navigate the period of losses while Lemonade advances its machine learning models to reduce the loss ratio below its target. This is likely a Plan B since it will mean sharing upside with such a partner who would be looking to access Lemonade’s core technology. Such strategic partners may wait to take over distressed assets later, but in a competitive marketplace, it seems at least one strategic partner would make an offensive move against their legacy competitors.

Best,

Stephen

I’m long AMZN, LMND, SQ and TSLA mentioned in this post. Nothing in this post is intended to serve as financial advice. Do your own research. The opinions and views expressed in this newsletter are those of the author. They do not purport to reflect the opinions, views or policies of any other organization, company or employer.