[E3.2] How Steve Jobs Disrupted Intel

Taking on moats and walled gardens

I’m writing this profile in Product | Strategy | Innovation after sharing insights into unit production cost declines and operating leverage in the last profile [E3.1]. These attributes contribute to what makes Amazon and Tesla so disruptive in their respective markets. This week we will expand on those insights in a second profile covering Disruptive Innovation theory by the late Professor Clayton Christensen at Harvard Business School. We will explore Apple as the disruptor to Intel as their established supplier to illustrate Christensen’s theory over a recent 7 year period across multiple computing platforms. Disruptive innovation also contributed to Sony’s success in the 80s and 90s, Toyota’s success entering the US market with the Corona in 1965 and Nucor taking market share from established steel companies over many decades starting in the mid 70s.

3 primary topics are discussed in this profile:

User needs, value networks and their influence on disruption

Customer (Apple) disrupting a key supplier (Intel)

Disruptive Innovation across multiple value networks

In a third profile, we will leverage key learnings from the first two profiles in this series to illustrate how we can disrupt the healthcare status quo with better access and lower cost while also improving outcomes. We will use a model to vaccinate the US population during a pandemic as a key use case. Future profiles will explore the full digital innovation stack in healthcare that spans health, medicine & therapeutics.

Background

Disruption, disruptors and the disrupted are terms used widely today across many contexts and to some extent they are also overused. These terms are side-effects of a theory that has evolved out of research by the late Professor Clayton Christensen at the Harvard Business School. Professor Christensen studied the success and failures of many market leading companies. A key tenet of disruptive innovation is these benchmark companies can do everything right and still lose market leadership over time when market dynamics change. This is often the result of new technologies entering that market or the market finding lower priced technologies elsewhere.

The Innovator’s Dilemma: When New Technologies Cause Great Firms to Fail was published in 1997 by Professor Christensen to describe his theory, provide background context on the computer hard disk drive industry and outline how to manage technological change. A case study into developing and commercializing a hypothetical electric vehicle is also presented. Understanding the market for electric vehicles combined with product, technology and distribution strategies highlights the role disruptive innovation plays to lead technological change. Disruptive innovation has been used since the concept was first introduced to describe many company failures like those of Digital Equipment Corporation and Blockbuster plus company successes like Nucor, Sony and also Toyota’s market expansion into the US market.

Since releasing The Innovator’s Dilemma, Professor Christensen published related works on The Innovator’s Solution, Seeing What’s Next, The Innovator’s Prescription and others such as many case studies on the topic with Harvard Business School Publishing. The upmarket migration of minimills like Nucor is extremely descriptive in The Innovator’s Solution. Minimill gross margins and the proportion of total steel production increased significantly to the upside as the steel quality improved with technological enhancements. For example, when the steel quality was only good enough to produce rebar, gross margins were 7% and the proportion of steel production was 4%. When the steel quality increased and minimills could sell competitive sheet steel, gross margins increased to 25-30% (7x rebar), but the proportion of steel production increased dramatically more to 55% (13x rebar).

1. User needs, value networks and their influence on disruption

Companies seeking to maintain or increase market leadership often engage customers for feedback to evaluate their needs. This can lead to selection bias with the best customers who are willing to pay more for new features to achieve better product performance. This can yield an upward migration in price and product complexity as scope expands beyond the original design. Customers that don’t really want or need these improvements are brought along for the ride whether they want these new features or not. That is until a disruptive technology comes along with 3 key value propositions:

provides only the performance they really need,

realizes the simplicity they prefer, and

costs 20-50% of their current solution.

The end result is some customers switch to the disruptor and the established supplier is disrupted. If this scales, the established supplier loses market share or worse.

Blockbuster

Blockbuster rented movies and other videos to consumers with the convenience of a neighborhood retail network with stores across the country. Thousands of Blockbuster stores offered movie rentals for $2.99 and the whole family could watch for this fixed price vs. movie theatre tickets purchased for each person (family of 4 x $10 per ticket is $40). The Blockbuster stores also offered extensive snacks to purchase with a movie rental, video games with consoles for a weekend if needed and somewhat of a social scene on weekend nights. But the videos also had to be returned to the store within a few days to avoid late charges. This became annoying when returning videos was inconvenient or you wanted to watch the movie again after the due date.

Netflix

Netflix entered the market with a broader selection of movies and a shipping arrangement with the US Postal Service to deliver and pickup DVDs direct to customer homes. You could keep a video as long as you wanted with an active paid subscription. If you returned videos sooner you could watch more movies per month with the same flat rate monthly subscription. Netflix turned Blockbuster’s $200 million in annual late fees into subscription revenue by converting Blockbuster customers into Netflix subscription users. That was possible with the DVD format because it minimized shipping costs. Blockbuster offered convenience. Netflixed offered a pain killer. Blockbuster lost and filed for bankruptcy. Netflix had a $235 billion market cap as of the market close on January 29, 2021.

Value Networks

Other factors influencing market dynamics are supply chains, business models, regulations, distribution, product mix and market competitiveness that cultivate market norms. These norms define a value network. Higher unit volumes transacted through a value network usually lead to more process controls to maintain quality and reliability. The network can also have a selection bias towards more profitable, premium-priced products and services that serve the needs of the most demanding customers in the value network. These traits can also lead to friction for many companies. So another form of disruption is sourcing products from less complex value networks. This can also lead to awareness of new markets by these companies selling upmarket to new companies and the creation of new market opportunities. The end result is lower priced products being used by less demanding customers.

User Needs

Users adopt products and technologies differently. This drives what is called the diffusion of innovation with early and late adopters. But some users might be over-served by a solution. They would adopt sooner if the solution aligned more closely with their specific needs at a lower price. This is illustrated in Fig. 3.2-1 if we assume a bell-shaped curve to model customer demand vs. a range of performance from low (left side) to high (right side). The mean represents peak user demand for a specific level of performance. Users who demand greater performance and are willing to pay a premium for those capabilities are located above the mean at maybe +2 standard deviations (SD) or greater. This would represent only about 2.25% of users, but if they pay substantially more for this greater performance, they might represent 10-15% of revenue. However, another group shaded in red at maybe -1SD (15.85% of users) would prefer to pay less for lower performance if the solution still meets their critical needs.

2. Customer (Apple) disrupting a key supplier (Intel)

Intel Corporation has a long history as a leading manufacturer in the microprocessor industry supplying computer manufacturers with these key components. The x86 instruction set processor family was first introduced in the late 70’s as a 16-bit extension of Intel’s 8-bit 8080 microprocessor. Recent x86 Intel processors can support 512-bit designs. These microprocessors have historically been used in computers where the primary use cases are desktop and portable contexts with power from a wall outlet. Rechargeable batteries for more mobile computer designs have driven a desire for lower power requirements for processors used in these computers. Reduced weight is a key objective for mobility and a limiting constraint to adding battery capacity to extend time on a charge.

Data centers drive premium pricing for their computer platforms. Data center customers likely drove Intel’s x86 processor specification bias upmarket to meet their demands and willingness to pay more than a consumer for a notebook computer. Intel did tier their processor product line to allow for more specialization and product positioning aligned with key segments. Apple transitioned to Intel x86 processors for the Macintosh line of computers in 2006. This was a major move for Apple to establish the Mac as a dominant computing platform for consumers and businesses with a proven Mac OS X Unix operating system built on top of leading Intel x86 microprocessor technology.

Apple

Steve Jobs launched the iPhone to the world in 2007. The video above is a masterclass on storytelling and launching a new product. Apple positioned the iPhone as a premium priced product, but the step change up in performance and features made it a telecommunication platform that disrupted owning multiple devices to match the capabilities of an iPhone. This reduced the total cost of ownership to obtain all these capabilities and was eventually wrapped into a monthly data plan through cell service carriers. The platform has become increasingly disruptive as third-party apps continue to optimize functionality to user needs. The rate cumulative unit production has scaled for the iPhone is much higher than for other recent computing platforms. Fig. E3.2-2 shows the relative rates Apple products hit 50 million cumulative units sold and higher. The iPhone surpassed 150 million cumulative units in less than 5 years. That means Wright’s Law presented in profile [E3.1] favored the iPhone to drive “System on a Chip” investments and innovation with each product generation due to the operating leverage created.

Apple needs to manage power consumption for these mobile devices to extend time on a charged battery. The iPhone uses multiple processors, but for the first 3 generations, Apple partnered with Samsung to produce an ARM processor to handle Applications like running iOS and iTunes and a separate baseband processor to handle the core phone functionality with cell towers. Apple brought the design of the iPhone A4 processor in-house with the iPhone 4 using its own ARM processor design (0.8-1GHz, single core, 32-bit). The A4 processor was also used in the original iPad, 4th generation iPod Touch and 2nd generation Apple TV.

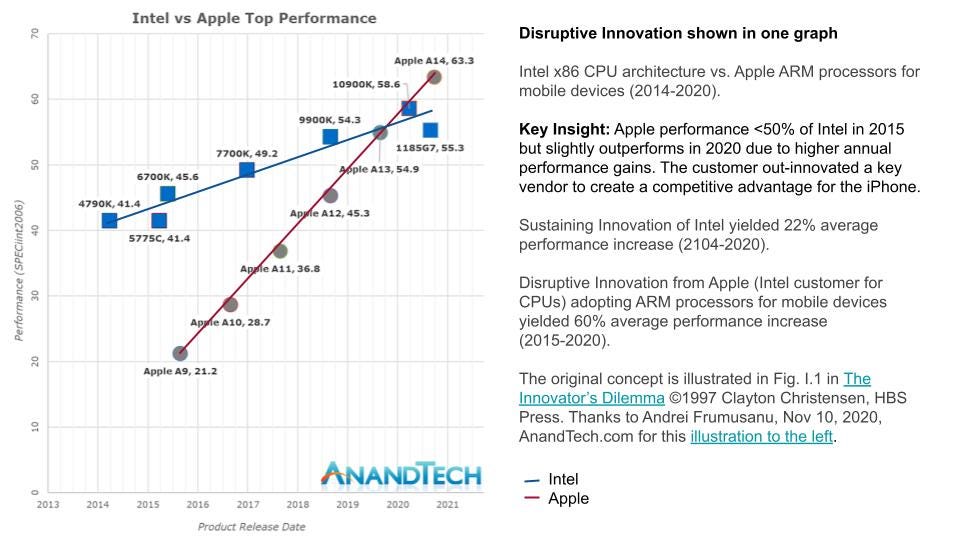

With each new generation of the iPhone, a new A-series processor enabled much of its new functionality. The latest iPhone 12 uses an A14 Bionic processor design (2.99 GHz, six-cores, 64-bit, quad-core GPU plus 16-core neural engine) based on 11.8 billion transistors. The accelerated rate of innovation for A-series processors has also enabled Apple to look beyond mobile devices like the iPhone and into other platforms. Fig. E3.2-3 shows the performance over a recent seven year period for representative processors for mobile devices from Intel and Apple. The performance of the Apple A9 processor was less than 50% of the performance of the Intel processor in 2015. However, in 2020, the performance of the Apple A14 processor outperformed the comparable Intel processor. Apple’s lower starting performance and faster rate of increasing performance over time are the hallmark features of disruptive innovation within the same value network.

3. Disruptive Innovation across multiple value networks

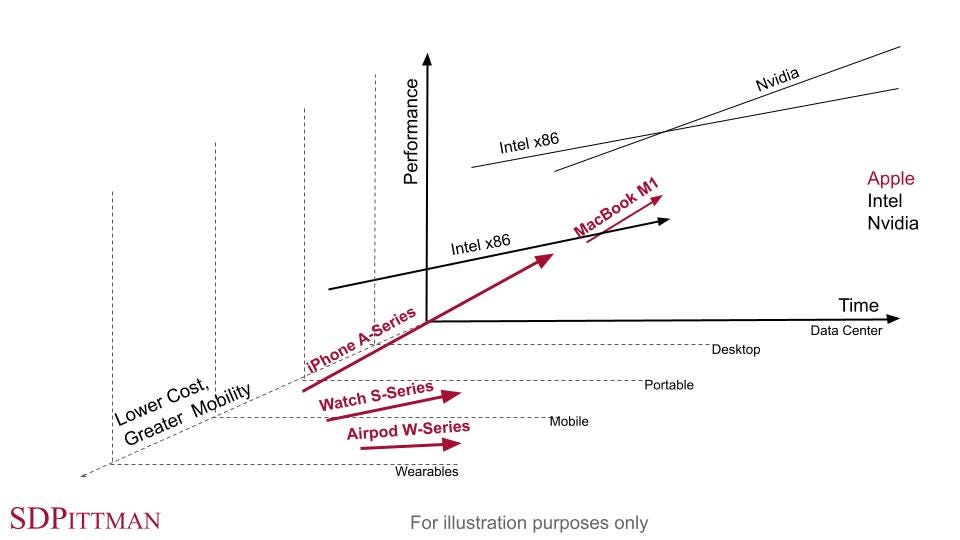

As Apple built competencies to design state-of-the-art ARM processors for Systems on a Chip, Apple was not limited to managing the power consumption for mobile devices. Multiple cores, neural engines and GPUs integrated into Apple’s processors provide enhanced capabilities to improve portable and desktop platforms, too. Apple introduced the M1 chip for the Macbook Air, Macbook Pro and Mac Mini in 2020 with performance greater than most standard laptop PC chipsets. This ability to design processors across multiple technology platforms outside of the data center gives Apple incredible flexibility to tier capabilities and product positioning for different degrees of mobility, performance and cost.

Although Apple may sell these hardware platforms using very similar business models and distribution, each hardware platform does have a specialized ecosystem of developers and subject matter experts that support each with some overlap of course. These hardware platforms span the following value networks:

Wearables (AirPods, Watch)

Mobile devices (iPod touch, iPad, iPhone)

Portable devices (Macbook Air, Macbook Pro, Mac mini)

Desktop devices (iMac, Mac Pro)

Data Centers (Cloud software services: iCloud, App store, Apple Music, Apple Arcade, Apple TV+, Apple Fitness+, Apple News+)

One striking feature about Apple’s Cloud software services is the breadth and reach these have across multiple hardware platforms from Airpods, Apple Watch & Apple Music for fitness to iMac & iCloud for editing videos and photos taken on an iPhone. If Apple can enhance the customer experience for all of these subscription services by vertically integrating its microprocessor expertise into the data center, it will certainly do so. In other words, just as Tesla owns the entire end-to-end customer experience with vertical integration from digital marketing, purchase, vehicle manufacturing, insurance, charging stations and autonomous navigation, Apple could also provide the entire hardware and software stack from Airpods to mobile devices and the data center that hosts and streams the apps, music, news, fitness programs & TV you use throughout the day.

Professor Christensen would graph the ARM processor chipsets in three dimensions across multiple value networks where the X-axis is time, the Y-axis is performance and the Z-axis projecting out of the page (or computer screen) is lower cost. Cost is a useful variable to segment this total ecosystem, but mobility also increases with Z, too. Therefore, the data center with the highest costs and least mobility is on the plane of the page (Z=0) and wearables such as AirPods have the lowest cost processors and the most mobility. This concept of 5 independent value networks connected with an evolving Apple processor family is illustrated in Fig. 3.2-4. What is so striking about this story is over approximately 10 years starting in March 2010 with the A4 processor, Apple already spans wearable, mobile and portable devices starting with the iPhone. This was intentional. The rapid growth and release schedule for new iPhone models and related Apple mobile devices provides a competitive advantage for Apple to continue to reinvest into their processor technology roadmap. Those investments are then leveraged across multiple platforms and value networks. And if Nucor is a proxy, peak Apple may occur once it enters and dominates the data center.

Conclusion

Disruptive Innovation is a key theory to better understand how products compete in the market and the strategies that drive business decisions and competitiveness. It also highlights the dilemma many companies face. Intel understands disruptive innovation. When Andy Grove was Intel’s CEO, he leveraged Professor Christensen’s theory and research to develop and launch the value-based Centrino processor. Grove’s rationale was protect Intel from unchecked disruption from competitors in this value-based segment. It worked and Intel maintained much of its dominance.

Intel even partnered with Apple later to provide processors for its Macintosh computers. But when Apple released the A4 processor, Intel had limited options to respond when Apple was such a dominant brand in the mobile devices segment. Intel could also likely predict the final chapters of the Apple microprocessor playbook. In those chapters, Intel is written out of Apple’s microprocessor future. That’s disruptive. That’s a walled garden destroyed.

In August 2020, Intel CEO Bob Swan announced the company was accelerating and had completed $17.6 billion of a $20 billion stock buy back program Intel announced in October 2019. That’s financial engineering. Apple responded with the A13 Bionic and A14 Bionic processors manufactured by Taiwan Semiconductor. Bob Swan’s tenure as Intel CEO ends February 15, 2021. Intel’s past CTO and recent VMWare CEO Pat Gelsinger will take over as Intel CEO on February 15, 2021. Gelsinger has a huge challenge to win back lost microprocessor market share from competitors like AMD, Nvidia, ARM & even Apple. But it seems the Intel Board of Directors is prioritizing innovation again.

The next profile in this 3-Part Series in Product | Strategy | Innovation will expand on disruptive innovation across multiple value networks with a focus on healthcare. Disruption has advantages with fragmented marketplaces and inefficiencies because of a pull effect towards less complexity if it reduces friction.

If you are not a subscriber, please consider doing so to get updates on this topic and more. Subscribers have early access when content is released. Consider the email copy the first draft that may evolve over time in the online archive.

If you liked this post, please share with your networks so others can benefit, too.

Nothing in this post is intended to serve as financial advice. Do your own research.