[E9.2] Improving Outcomes with Connected Care

More SIGNAL, less NOISE, Virtual Care FIRST

Dear Reader,

This Profile in Product | Strategy | Innovation continues a 3-Part Series on a Health Ecosystem and model to describe it. Our focus here is to inform Strategy and Innovation. In Part 1 of the Series, we provided an overview for a 3-Pillar model covering this Health Ecosystem. Then we followed up with an Update on Digital Health to provide more context on what we will cover on Improving Outcomes with Connected Care.

Healthcare is one of the largest markets with an estimated global market cap reaching $12 trillion by 2022. Healthcare remains fragmented with many incumbents and new ventures. We need emerging disruptors to drive change for improved outcomes and greater efficiencies to also lower total costs. We need something different.

In this Part 2 we will cover:

Virtual Care FIRST as a catalyst for change,

Digital Medicine to integrate continuous care, and

Digital Therapeutics to enhance outcomes.

These 3 topics provide insights and context into Improving Outcomes with Connected Care. But what exactly is Connected Care?

Background

On a fundamental basis, Connected Care covers system integration like medical devices and systems inside hospitals on common platforms to share and analyze health data on monitored patients. Connected Care through this lens can “see beyond the obvious” to anticipate changes in health status on a patient before providers are even aware of a change. Onsite edge computing connected to cloud services makes this possible. Communication between providers happens on private networks and health data are stored in a private records to further connect care.

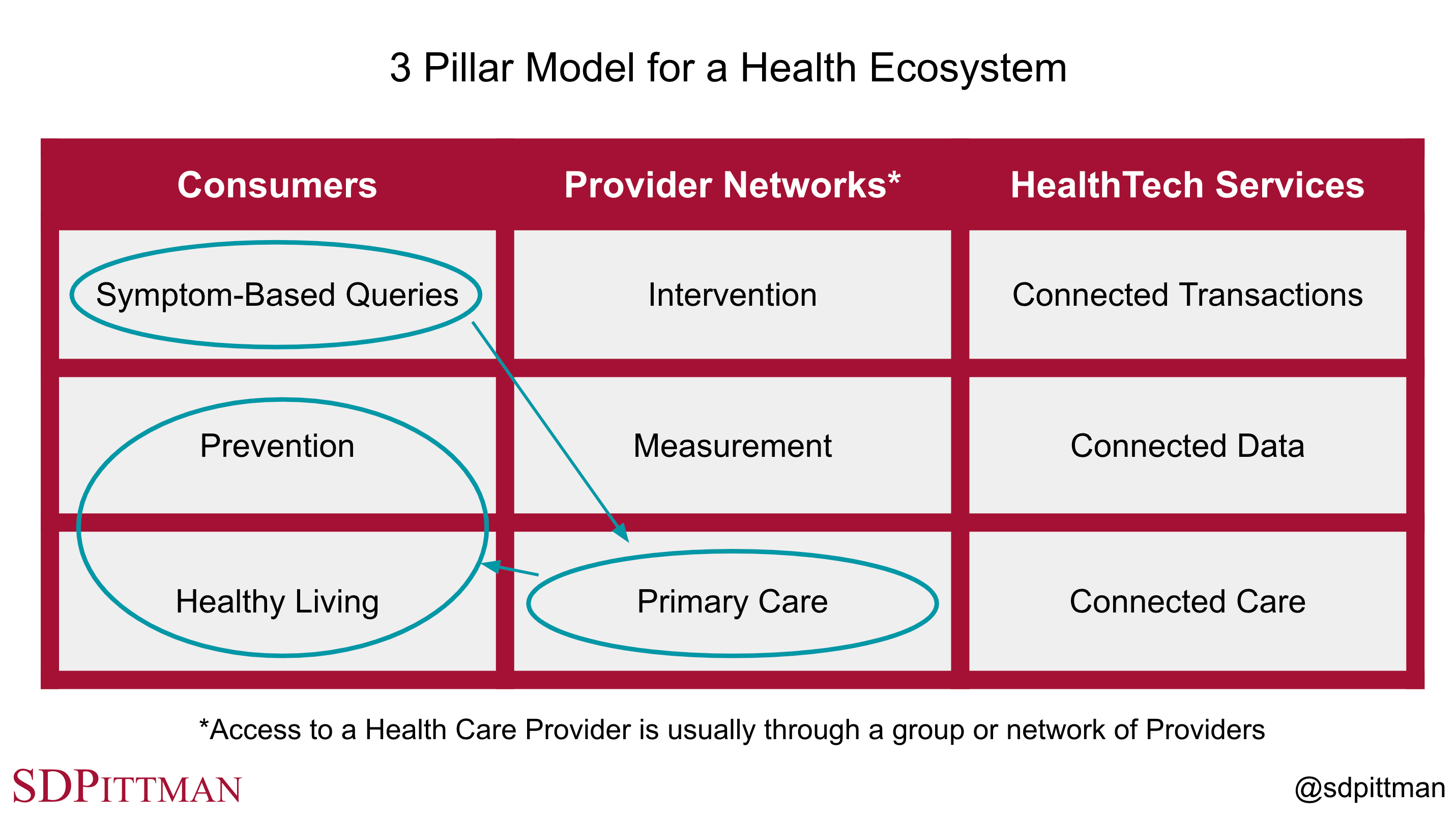

But on a much broader scale to build a viable Health Ecosystem, Connected Care should enable the entire range of solutions required to improve health outcomes and positioned at different price points. These solutions should also provide different ways to access services. Connected Care is highlighted in our 3 Pillar Model as 1 of its 9 domains of innovation as part of the HealthTech Services Pillar shown in Fig. 9.2-1. These 3 vertical Pillars represent a Health Ecosystem that forms a marketplace between Consumers and Provider Networks. HealthTech Services enable this marketplace to provide care, leverage data and transact business. A viable Health Ecosystem should also allow Consumers to access many products and services without the need to access Provider Networks.

Connected Care goes from 1 domain in the 3-Pillar Model to the added detail illustrated in Fig. 9.2-2 with 2 dimensions spanning access to care horizontally and across a digital health stack dimension vertically.

At least 3 dimensions are needed to represent solutions this way.

One dimension provides a Digital Health Stack consisting of Digital Health, Digital Medicine and Digital Therapeutics.

Second dimension provides 3 core ways to access care as a Consumer, through an Employer or through a Provider Network.

Third dimension provides an xTech Stack to represent the fundamental technology layers that makes up a solution. Digital is the primary layer that connects the solution to other services. The other layers are more solution specific as shown in Fig. 9.2-3. The x in xTech represents MedTech where FDA-cleared solutions match the 4 orange domains in Fig. 9.2-2. HealthTech is the xTech for the 5 light grey domains in Fig. 9.2-2 where solutions may exist outside of FDA regulations or just require registration without a submission for clearance.

The figures presented above illustrate how a simple model of a Health Ecosystem can expand into multiple dimensions to integrate complex systems into solutions to advance Connected Care. These solutions leverage Provider Networks and relevant companies to deliver Interventions against the market needs and product requirements. But viable Ecosystems also activate Healthy Living and Prevention to reduce the need for Intervention through Provider Networks over time. This is possible when communities build and scale a 2-sided marketplace between Consumers and Provider Networks just as Block (previously Square) is building a marketplace between Sellers (restaurants, retail shops and other small businesses) in a community and Consumers using Cash App. Virtual Care FIRST is a catalyst at scale to drive community-based ecosystems around both Health Living and Prevention with Consumers. This represents change.

Also, Fig. 9.2-3 represents how gene sequencing, cell cultures, tissue and organ transplants, drugs and implanted devices are integrated through a digital platform into Connected Care. Liquid biopsies are possible to screen for cancer with the detection of circulating tumor DNA with a routine blood test. These tests may eventually become a part of Primary Care with Measurement in high-risk patients based on family history and even broader cohorts of patients. And pacemakers used to treat heart failure are connected to health care providers to detect changes in status with Measurement to guide the need for Intervention.

1. Virtual Care FIRST as a catalyst for change

Anthem President and CEO Gail Boudreaux mentioned on Anthem’s 2021 third quarter earnings call Anthem is offering “virtual care first” as part of health benefit plans sold to large employers in 14 states. At the time of the earnings call on October 20th, 50 national accounts representing 900,000 commercial members had signed up for virtual care first services to improve access to care and convenience for their employees with a digital platform called Sydney Preferred.

Anthem is also an investor in K Health, a digital and virtual care service with over 5 million direct-to-consumer users. And Anthem is also an investor in a new joint venture between K Health, Blackstone Growth and Anthem called Hydrogen Health to provide virtual first commercial health plans direct-to-employers and direct-to-health-plans leveraging K Health’s AI Engine and health care providers across urgent care, primary care, mental health, and pediatrics. These investments and partnerships align Anthem across various ways to access care as shown in Fig. 9.2-2.

K Health is aligned with access for Consumers.

Hydrogen Health is aligned with access for employees (cohorts of consumers) through their Employer using K Health assets to service those employees.

Anthem is aligned directly with Provider Networks to deliver care to Anthem’s members.

Members come to Anthem either through traditional health benefit plans (primarily through employers, medicare or medicaid) or through the emerging virtual care pathway using K Health, Hydrogen Health and others. Anthem’s digital service known as Sydney Health is focused on improving access and convenience for its members.

Virtual primary care is offered by a growing number of health services like Firefly Health, HealthTap, Sesame, Teladoc, Amwell, Walmart Health, CVS Health, Anthem, UnitedHealthcare Group, Aetna, Oscar, Lemonaide, and others. The pandemic has accelerated the adoption and growth of virtual care. But this growth has transformed an e-visit or telemedicine by your own primary care provider as needed into the transformation of a totally new way to deliver health services that is virtual first. For medical emergencies, individuals would still call 911, but for urgent care, a virtual care visit online or through a mobile app can initiate triaging symptoms first digitally and then with a provider as needed.

At scale on national basis, this will evolve to include local partner facilities and services to complete any needed exams, medical tests or labs to guide clinical decisions. Virtual Primary Care is more integrated and comprehensive than a telehealth video chat. Digital Health, Digital Medicine and Digital Therapeutics will also play key roles to integrate care between virtual Primary Care visits and Measurement and Intervention through local Provider Networks.

Looking at virtual Primary Care through the Connected Care lens, we see digital platforms disrupting legacy health care with digital agents automating the leading edge of triage direct to the individual to define primary symptom(s). This might even happen with a Consumer just curious to better understand their symptoms as illustrated in Fig. 9.2-4 with a Symptom-Based Query. Services like the K Health chatbot can help individuals investigate an issue in less than 10 minutes at no cost to then take action if recommended and desired. That could then lead to a virtual primary care visit on-demand with a Provider for a fixed fee. For many issues like a urinary tract infection, headache, dental infection and many other conditions, a provider might be able to prescribe medication or recommend other treatments during the virtual visit and even offer home delivery for a prescribed medication. Think DoorDash for Primary Care!

Healthy items on menus that meet “great health” criteria for both ingredients and portions should look like NASCAR with national brands subsidizing some of the cost.

If 30-40% of primary care visits could be handled virtually first, this not only adds convenience and saves cost, but also frees up primary care and urgent care resources to focus more on individuals that need in-office visits. This also decentralizes access to care when care can happen in the home or workplace. An extension of this decentralized access to care for Consumers (and groups of Consumers through Employers) is Healthy Living and Prevention to disrupt the need for primary care. Virtual primary care visits can address the primary symptom that led to the consult, but can also activate a healthy living plan for the Consumer to follow along with any programs available in the community as illustrated in Fig. 9.2-4.

Payers like Anthem and UnitedHealthcare Group and large self-insured employers in a community can incentivize Healthy Living and Prevention by discounting virtual primary care when physical activity and behavior metrics are met. Additional incentives in a community are possible with rewards for documented physical activities like walks, bike rides and VR challenges. Sponsored healthy meals in the grocery store and restaurants emphasize healthy nutrition.

Instead of brands advertising primarily on media like TV, Google, and Facebook, healthy items on restaurant menus that meet “healthy nutrition” criteria for both ingredients, preparation and portions should look like NASCAR with national brands subsidizing some of the cost. This could include both a fixed monthly subsidy to the restaurant and a customer-specific subsidy if the customer has proof they are in a participating virtual care first program. These incentives could also accelerate the adoption of virtual primary care.

Mental Health and Pediatrics will also benefit from a virtual care first strategy. Mental Health in particular needs attention when the issue is acute, but not a crisis. A mental health crisis should always have access to a crisis center or an emergency response either directly or as a virtual care visit evolves. But bouts of anxiety and depression can benefit when acute by talking to provider or trained professional. A provider can then activate a virtual treatment plan.

2. Digital Medicine to integrate continuous care

Provider Networks form the middle Pillar in Fig. 9.2-1 to create a marketplace with Consumers. Providers deliver Primary Care, but regulated Measurement and Intervention are key tools differentiating care from a licensed provider. Connected Care not only connects Consumers to Providers, but also connects primary care providers to specialists or digital platforms with comprehensive solutions. Managing diabetes requires monitoring blood sugar levels. Low cost glucose meters require lancets to prick the finger to draw blood and test strips to collect a blood sample for analysis by the meter. Many of these are available today at relatively low cost without a prescription for use by consumers.

Continuous glucose monitoring (CGM) devices provide Digital Medicine with a wearable sensor measuring blood sugar usually every 5 minutes, 24 hours a day and transmits this blood sugar level to a wearable receiver, mobile app or insulin pump. These data are easily shared with providers and their care teams to help provide more insights into the underlying physiology. This allows more personalized coaching on nutrition, sleep and exercise to help regulate the blood sugar level using the CGM trends.

Our pancreas helps to regulate blood sugar by secreting insulin when blood sugar is high and secreting glucagon when blood sugar is low. An artificial pancreas would monitor blood sugar and then regulate blood sugar by administering insulin and glucagon. The control of such a system needs to be sophisticated to prevent runaway with over administration of both insulin and glucagon. External systems can represent key features of an artificial pancreas.

Digital Medicine enables closed-loop control when Measurement drives Intervention as shown in Fig. 9.2-5. Insulet in Billerica, Massachusetts has conducted clinical trials for an investigational device it calls the Omnipod 5 (OP5) as a hybrid closed-loop system to manage diabetes. Third party CGM wearable devices from leading companies like Dexcom (wearable on the right of Fig. 9.2-5) provide a trend in the blood sugar levels for Measurement. A controller used as a stand alone device or eventually as an app on a smart phone analyzes the blood sugar trend with algorithms and provides features like HypoProtect to prepare the system in advance of when the user plans exercise so the system can respond appropriately. The Omnipod wearable (left side of Fig. 9.2-5) is a tubeless insulin pump that attaches to the skin usually around the abdomen to administer insulin with feedback from the controller or directly from the CGM wearable.

Many individuals manage diabetes with the conventional finger prick, blood glucose meter and insulin injection if needed. This is the Volkswagen of diabetes management. Type 1 diabetes or difficult to control type 2 diabetes may eventually need an implanted artificial pancreas from Boston-based Beta Bionics to monitor blood sugar and administer either insulin and glucagon based on the need. This is the Porsche of diabetes management. But the real innovation will happen with external wearable approximations of an artificial pancreas. These systems are the Audi with more capabilities than a Volkswagen, but more cost effective than a Porsche. Insulet, Dexcom, Medtronic, Abbott, Eli Lilly, Sanofi and Novo Nordisk will all play a role to drive innovation within Digital Medicine to manage diabetes.

Connected Care will advance the systems used and the targeted interactions providers and their teams can provide to patients with access to the data generated by these systems. This includes virtual integration between primary care and specialists that may include obesity medicine, endocrinologists, registered dietitians, exercise physiologists, sleep specialists, behavioral psychologists and patient advocates. And at the limit, Connected Care includes access to Consumer who may be having the leading edge of symptoms for diabetes who use Symptom-Based Queries in Fig. 9.2-1 to better understand their issue and are connected to Primary Care to activate a Provider Network in their community.

Software-as-a-Medical-Device (SaMD) also plays a role that fits into the model for Digital Medicine as part of Connected Care. Apple Watch 4 and later versions include a digital crown to return to the home screen, zoom and scroll. The digital crown also acts as an electrode to capture a single channel electrocardiogram (ECG) if a user downloads the ECG App. The ECG app is regulated software that makes the Apple Watch 4 or later and ECG app a Class II medical device to record and save a single channel ECG and check the recording for atrial fibrillation (AFib), a form of irregular rhythm. If AFib is detected, it is recommended for users to schedule an appointment with a cardiologist or another qualified provider to evaluate further with a more comprehensive examination and diagnostic test. Digital Medicine will continue to evolve in areas where wearables integrate into medicine to provide better care.

3. Digital Therapeutics to enhance outcomes

Digital Therapeutics are gaining traction with an expected global market size just over $10 billion by 2025. But this traction must be based on better outcomes compared to standard of care. Fig. U26-1 in a recent Update on Digital Health shows the relationships and differences between the different categories including Digital Therapeutics.

Digital Therapeutics drive evidence within Digital Health to mitigate potential risks with more regulatory control and real-world outcomes. In many cases there is no predicate to use as a proxy for a specific Digital Therapeutic and the intended use, so a de novo submission may be required to pursue FDA clearance for marketed claims in the United States. The rigor for these submissions is much greater because not only are you validating the system design with outcomes in clinical trials, but you are also negotiating the law that will govern use of the therapeutic for others to follow using your submission as their predicate. The bar is high.

Many Digital Therapeutics on the market or in development target specialty care. These improve care downstream from Primary Care and may even provide the Intervention for Digital Medicine. But some Digital Therapeutics provide upstream opportunity right at the point of virtual Primary Care FIRST. One example is Somryst from Pear Therapeutics for chronic insomnia (difficulty falling asleep) as a prescribed digital therapeutic (PDT). Somryst includes 6 clinically-validated lessons delivered on a mobile device over up to 9 weeks under the supervision of a licensed health care provider. Restricting sleep may be required as part of the Intervention. This requires supervision by a provider.

Mobile apps can be designed to engage users more than paper brochures and booklets. Somryst is based on clinical evidence generated over many years using cognitive behavior therapy. But Somryst studies (also conducted under the original name SHUTi) demonstrate not only sustained clinical outcomes at 12 and 18 months compared to a control group, but also early detection of patients at risk of dropping out of therapy for intervention by a clinician.

A challenge Somryst faces is a competitive marketplace for chronic insomnia with a global market size of $5.4 billion by 2023. Pharmacotherapy includes both proprietary and generic medications. And even in the digital therapeutic space, Somryst competes with the non-prescription digital therapeutic sold through employers as a benefit for problem sleep as Sleepio from Big Health. Sleepio also has clinical evidence supporting claims as is less expensive than Somryst in most cases. But adoption of PDTs by payers is still early and as adoption scales the price will likely follow Wright’s Law with a decrease in cost as deployments double to help drive down price. This is due to the efficiencies of digital solutions especially if they are software only where fixed costs are spread over all users and variable costs collapse with scale. But this requires millions of cumulative patients on a PDT platform versus thousands with early adoption.

Digital Therapeutics will gain traction where managing chronic disorders improves with more dynamic, continuous care and patient engagement. Mobile apps are routine today, but wearables integrated with mobile apps and virtual reality will drive even more control and engagement. Mental health, clinical neuroscience including pain management, gastrointestinal disorders and diabetes are some examples of large markets where digital therapeutics are gaining adoption or have potential to scale.

Conclusion

Block (previously Square), Spotify and Amazon are proxies for Connected Care with global scale for an ecosystem on a connected platform to drive down user costs. Block in particular combines that scale with local small businesses to form a marketplace between Cash App users and Sellers made of restaurants, retailers and others. Virtual care through companies like K Health is the Cash App equivalent. When Consumers engage the K Health app and chatbot with symptoms they become more informed at no cost. If they connect virtually to a health care provider that is similar to converting cash in Cash App to Bitcoin for a transparent fee. And if they follow-up with a local provider that is like the Cash App user going into a participating restaurant and using Cash App to pay for the meal.

If virtual Primary Care improves access, convenience and efficiency at lower cost, Symptom-Based Queries are the scalable, free solution to engage Consumers. Now if communities can rally behind Consumers and Provider Networks to improve Healthy Living and Prevention, we can build sustainable infrastructure to improve health outcomes and lower cost. Otherwise, we will soon be spending 25% of our US economy on health care. That is not sustainable. We need more Uber for health care and less Porsche.

Digital Health with it categories that include Digital Medicine and Digital Therapeutics also offers advantages with Connected Care. At scale, virtual Primary Care in some cases may be able to directly prescribe evidence-based Digital Therapeutics. Digital Medicine combines Measurement and Intervention with clinical evidence, wearables, mobile apps and in some cases pharmacotherapy. As Digital Medicine evolves to include integrated closed-loop systems, patients can take more control over their chronic conditions with a reduced need for interactions with providers although care will still be under supervision by a licensed provider.

Digital Therapeutics will be the most disruptive Digital Health category to pharmacotherapy and specialists at scale. Diabetes may be a proxy. As diabetes care has improved with standards of care, better glucose meters and improved ways to administer insulin, Primary Care now takes care of more diabetes. As Digital Therapeutics improve and scale, these will also be used in Primary Care. Digital Therapeutics become the “specialist” in a device.

Happy Holidays!

Best,

Stephen

I’m long AMZN, GOOG, SPOT, SQ and TDOC mentioned in this update. Nothing in this post is intended to serve as financial advice. Do your own research.