[U35] Moderna: all-in to commercialize synthetic biology

[U35] Moderna: all-in to commercialize synthetic biology

Can synthetic biology support both vertical (Moderna) and horizontal (Ginkgo Bioworks) integration strategies?

Dear Readers,

In the last Update in Product | Strategy | Innovation I reviewed the horizontal platform and integration strategy for Boston-based synthetic biology company Ginkgo Bioworks. In this Update, I will explore Cambridge-based synthetic biology company Moderna and their vertical integration strategy. Can synthetic biology support both strategies? Is one strategy favored over the other one?

I will start this Update with some context. The most valuable companies in the world today offer vertically-integrated solutions direct-to-consumers in large global markets even if products & services are also sold to businesses. These companies include Apple, Microsoft, Amazon, Alphabet and Tesla. Vertical-integration enables more control over their products & services to meet the needs of target customers and increase profitability by scaling more unit production and revenue over the same fixed-cost investments.

Tesla estimates it will invest $10 billion into Giga Texas to realize the innovation it has developed. These costs are carried by Tesla independent of how many vehicles are produced at the Giga Texas.

For example, Tesla’s new gigafactory in Austin, Texas includes manufacturing to die-cast large front and rear underbody segments as single parts, lithium-ion battery 4680 cell production and structural battery pack production. The latter integrates many battery cells into the mid-section underbody segment of the vehicle. These front and rear underbody segments and mid-section structural battery pack are then assembled to form the chassis of the Tesla Model Y manufactured in Giga Texas. Tesla estimates it will invest $10 billion into Giga Texas to realize the innovation it has developed. These costs are carried by Tesla independent of how many vehicles are produced at the Giga Texas.

Steve Jobs and Apple disrupted Intel by making an Apple-designed, low-power microprocessor for the iPhone. Over time, the Apple A-series microprocessors have continued to improve by focusing on the specific needs of customers using the iPhone. And now Apple has brought similar technology to the MacBook with the M-series of processors to further disrupt the core business of Intel on computers. The growth of the iPhone is also due to its use as a vertically-integrated platform with high-performance sensors for software developers to create leading apps that run on iPhones and iPads. These apps are also distributed to end-users through the Apple App Store.

And even though Amazon started as only an e-commerce company selling books online, over time it expanded the scope and scale of the products offered. Amazon started offering services it developed to create its own vertically-integrated platform to other businesses with Amazon Web Services (information technology and cloud-based systems) and Retail Marketplace (Fulfillment by Amazon). Amazon Prime was developed to monetize customer acquisition for Amazon and its strategic business customers.

COVID-19 presented a unique opportunity for Moderna and BioNTech to accelerate commercializing technology spanning significant discovery to pre-clinical innovation and limited clinical trial experience.

So it is not surprising Moderna would want to vertically-integrate its synthetic biology mRNA platform within the pharmaceutical industry as a biotech company. This spans discovery to pre-clinical innovation to human clinical trials to manufacturing commercial products and wholesale distribution. German mRNA platform competitor BioNTech SE partnered with Pfizer to scale clinical trials and commercialize its own COVID-19 vaccine. Moderna chose to raise the required funds through the capital markets to scale those same capabilities without a major pharmaceutical company partner.

The 2021 financials were similar between Moderna (Total Revenue: $18.5B, Gross Profit: $15.9B, Earnings Before Income Taxes (EBIT): $13.3B) and BioNTech (Total Revenue: EUR19.0B, Gross Profit: EUR15.1B, EBIT: EUR15.1B) with about 1.15 US Dollars to 1.0 Euros at the end of 2021. But Moderna’s brand certainly benefited more than BioNTech’s since Pfizer got more of the media mentions as the commercial partner for BioNTech. And Moderna worked closely with the FDA on the approval of its vaccine whereas BioNTech did that in partnership with Pfizer. But over time the robustness of the commercial pipelines for Moderna and BioNTech will determine the long-term success of their vertical-integration strategies.

Synthetic biology provides a window to watch 3 different corporate integration strategies evolve and perform over time

Synthetic biology has many definitions, but the basic concept is to use engineering principles to redesign existing natural biologic systems for a given purpose. The origins of synthetic biology date back to the 1970s with the development of DNA sequencing and synthesis. The first conference dedicated to synthetic biology was held at MIT in 2004. The field has continued to evolve and innovation has accelerated as the unit costs to sequence and synthesize genetic material continue to drop.

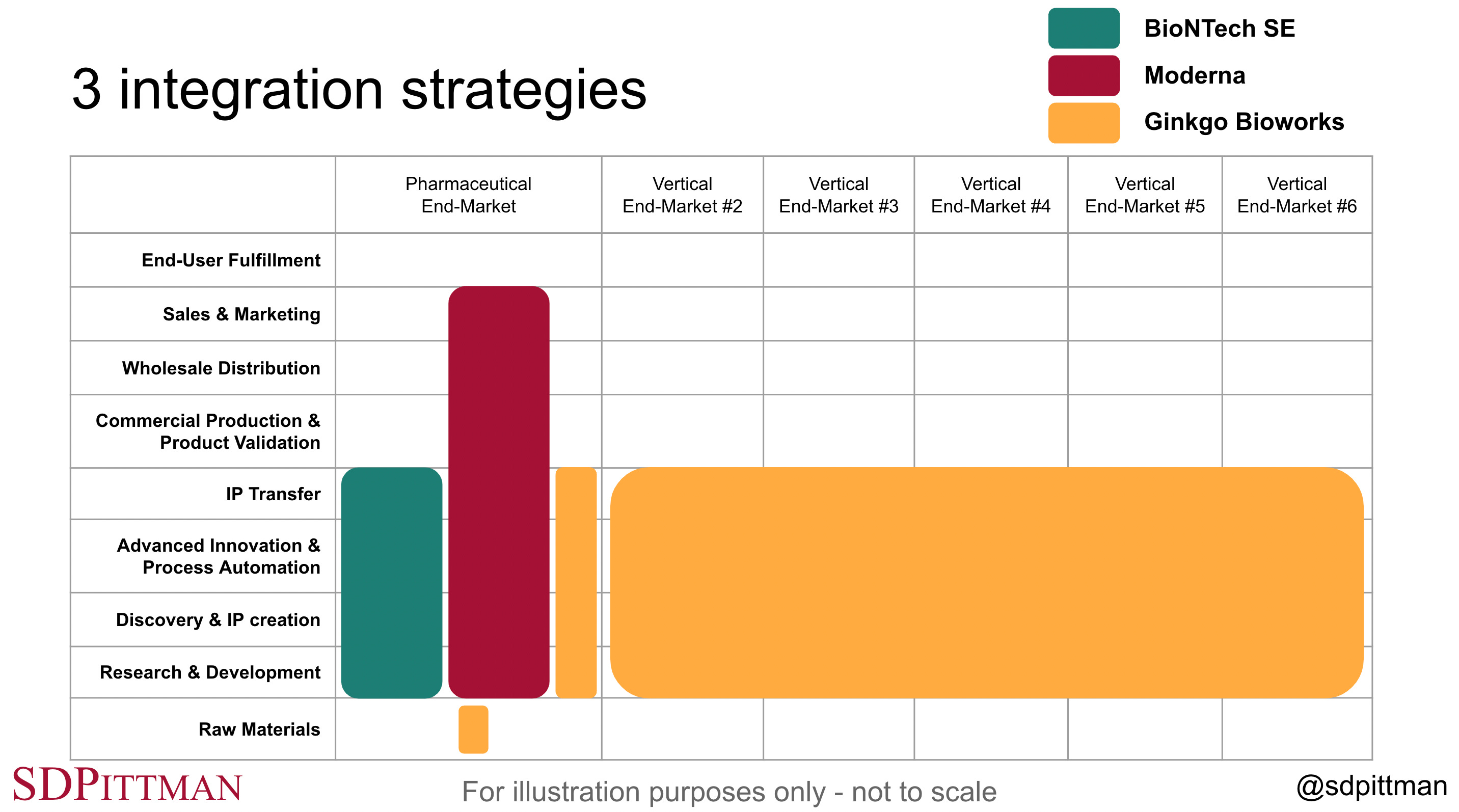

The figure above illustrates 3 integration strategies used by 3 public companies.

Vertical integration (partial) - innovation & IP transfer - BioNTech SE

Vertical integration (full) - innovation & commercialization - Moderna

Horizontal integration - innovation & IP transfer - Ginkgo Bioworks

BioNTech has multiple programs to develop IP to treat infectious diseases and cancer with 32 products in various stages of development including the Comirnaty vaccine for COVID-19.

BioNTech SE is pursuing a partial vertical integration focused on a commercial pipeline with innovation to create and transfer IP to another company. BioNTech partnered with Pfizer (global markets excluding China) and Fosun Pharma (China) to commercialize its multi-billion euro mRNA COVID-19 vaccine. BioNTech has multiple programs to develop IP to treat infectious diseases and cancer with 32 products in various stages of development including the Comirnaty vaccine for COVID-19. The infectious disease programs are currently focused exclusively on mRNA vaccines. The cancer programs span 4 drug class platforms with mRNA, engineered cell therapies, antibodies, and small molecule immunomodulators.

If BioNTech continues the strategy it used with Pfizer to commercialize Comirnaty outside of China for the COVID-19 vaccine, it will license other de-risked IP to a major pharmaceutical company or other third party to scale commercial production, design and run clinical trials, communicate with regulators and commercialize the product with regulatory approval. This does allow BioNTech to work on multiple drug class platforms across many programs if it continues to license the IP created to third parties. But it also means revenue is shared with these same third parties who successfully commercialize the products.

Moderna on the other hand is more focused on leveraging the full potential of mRNA science with 44 products in its pipeline at various stages of development including the Spikevax vaccine for COVID-19.

Moderna on the other hand is more focused on leveraging the full potential of mRNA science with 44 products in its pipeline at various stages of development including the Spikevax vaccine for COVID-19. Moderna also has 7 products in development related to COVID-19 and its variants. Moderna will likely continue to commercialize these vaccines for COVID-19 as a fully vertically-integrated synthetic biology company. Moderna has used third party vendors to scale production of the Spikevax vaccine due to the scale of manufacturing required, but Moderna leads all of its commercial activities. This also means Moderna keeps the profits to wholesale the final product.

Moderna has developed a proprietary, web-based mRNA Design Studio for the rapid design of multiple mRNAs. These can target a specific protein and allow digital modeling and simulations to test various assumptions. The mRNA Design Studio can order the synthesis of a specific mRNA design through Moderna’s automation platforms. Moderna uses its high-throughput mRNA pre-clinical production facility to manufacture the output of the mRNA Design Studio with delivery in just weeks.

Ginkgo Bioworks has stated it expects to onboard 60 new cell programs in 2022 with 508 new cell programs in 2025 within the vertical end-markets it currently serves.

Ginkgo Bioworks is pursuing a totally different corporate strategy than BioNTech and Moderna to commercialize synthetic biology. Ginkgo is building a horizontal platform for cell programming across at least 6 global vertical markets. But Ginkgo does share the focus on transferring IP like BioNTech to a strategic partner in a designated vertical who then commercializes the licensed IP into commercial products for a specific end-market. Ginkgo Bioworks has stated it expects to onboard 60 new cell programs in 2022 with 508 new cell programs in 2025 within the vertical end-markets it currently serves.

COVID-19 presented a unique opportunity for Moderna and BioNTech to accelerate commercializing mRNA vaccine technology for the first time. The 2021 financials for both companies realized significant upside as shown above with the emergency use authorization of their COVID-19 vaccines and the commercial rollout that followed. Ginkgo did not benefit as much because they did not have the right IP at the right time in the right vertical. But what if significant opportunities emerge across multiple verticals at different times with the right strategic partners to license the right IP?

The 2021 financials for Ginkgo Bioworks were Total Revenue: $313.8M, Gross Profit: $184.1M and EBIT: -$1.8B. And Ginkgo did commercialize technology in response to COVID-19 with the launch of a biosecurity business focused on COVID-19 diagnostic testing services and collaboration with Moderna to optimize production for some of the raw materials used in its vaccines.

Scope and Scale are more important than vertical versus horizontal integration

As already mentioned, vertical integration can help a company maintain more control over the supply chain for end products & services to meet the needs of target customers. If this is executed well it allows the scope of influence to expand to more target customers in existing or maybe even new markets. Success also leads to new products with the market intelligence gained from meeting the needs of target customers. As the scope expands with new markets, customers and products, the scale of core functions can also grow exponentially. Supply chains, production and business processes improve with ongoing innovation.

Fixed cost investments in this innovation also create operating leverage as unit production and sales are realized across exponentially growing scale to improve unit economics. Vertical integration is best suited to create this operating leverage across all the steps across the value chain shown as rows in the figure above. Moderna should outperform BioNTech as long as it can drive similar output in the early steps of R&D, discovery & IP creation with top talent and scope of products in development. The outperformance would be due to integrating more steps in the value chain from raw materials all the way through sales and marketing to the end-user fulfillment and dispensing. Moderna could be the synthetic biology equivalent of Tesla with enough vertical integration and operating leverage. This also assumes Moderna brings hundreds of products to market over 10-15 years.

Ginkgo has some disadvantages with horizontal integration. It will always share revenue with strategic partners and new ventures built on top of its platform. But Ginkgo can also grow across multiple verticals with the right strategic partners in each vertical compared to BioNTech that is partially integrating within only one primary vertical. Amazon Web Services is a proxy for the horizontal platform Ginkgo is building across multiple verticals. The scale of Amazon Web Services allows it to expand the scope of services with early adopters in one vertical and then roll out these services across all relevant verticals it serves.

Ginkgo announced on June 21, 2022 it reached its third productivity milestone target for tetrahydrocannabivarin (THCV) with strategic partner Cronos Group to produce eight cultured cannabinoids. Cronos launched its first cultured cannabinoid product in Canada from the partnership with Ginkgo after reaching the first productivity milestone in August 2021 for cannabigerolic acid (CBGA). And reaching the third productivity milestone resulted in Cronos issuing 2.2 million common shares of Cronos to Ginkgo.

Conclusion

Synthetic biology offers the biotechnology to bring potential breakthrough products to market across many verticals. Therapeutic and vaccine opportunities have attracted much of the attention for synthetic biology companies. Innovation and funded programs for mRNA vaccines put Moderna and BioNTech SE in the unique position to respond quickly to the COVID-19 pandemic. The result was strong financial performance for both companies in 2021. The cash on their balance sheets can accelerate additional programs to bring even more products to market. Both companies are actively working on multiple cancer therapies. To summarize:

If Moderna can expand the scope and scale of its vertical integration to innovate and bring 100s of new therapeutics and vaccines to market, it could become the Tesla of synthetic biology with scaled production, automated processes and talent across the value chain from Research & Development through Sales & Marketing.

If Ginkgo Bioworks can expand the scope and scale of its horizontal platform with 1,000s of cell programs across multiple vertical markets, it could become the Amazon Web Services of synthetic biology. The horizontal platform would be used to commercialize new products by many strategic companies in their respective vertical end-market.

If German BioNTech SE can expand the scope and scale of its vertical integration from Research & Development to transferring IP to strategic partners who commercialize 100s of new therapeutics and vaccines, it could become the Robert Bosch GmbH of synthetic biology. Bosch was the largest tier-1 supplier in the automotive industry in 2020 with 71.6 billion euros in sales.

Moderna is all-in on synthetic biology making large investments to build out its infrastructure and talent to commercialize the products it innovates. It accelerated these investments in response to the COVID-19 pandemic. Every product it brings to market can leverage many of these fixed-cost investments to realize operating leverage. BioNTech is working on similar technology platforms, but the pharmaceutical industry supports many large enterprise companies today. BioNTech is competing more to disrupt legacy platforms than head-to-head competition with Moderna alone.

And Ginkgo Bioworks is advancing synthetic biology with a horizontal platform across many verticals that are out-of-scope for Moderna and BioNTech. Thus, the opportunity for synthetic biology is large enough to support each of these companies and their integration strategies. They are disrupting other companies using legacy platform technologies versus each other within synthetic biology.

Best,

Stephen

Nothing in this post is intended to serve as financial advice. Do your own research. I’m long DNA, MRNA, and TSLA mentioned in this update.